Finro: The Best Startup Valuation Firm Built for Founders

Startup valuation is one of the hardest challenges founders face. The valuation of a startup does far more than assign a number to the business. It directly affects fundraising, determines how much ownership a founder keeps, and shapes how investors judge credibility.

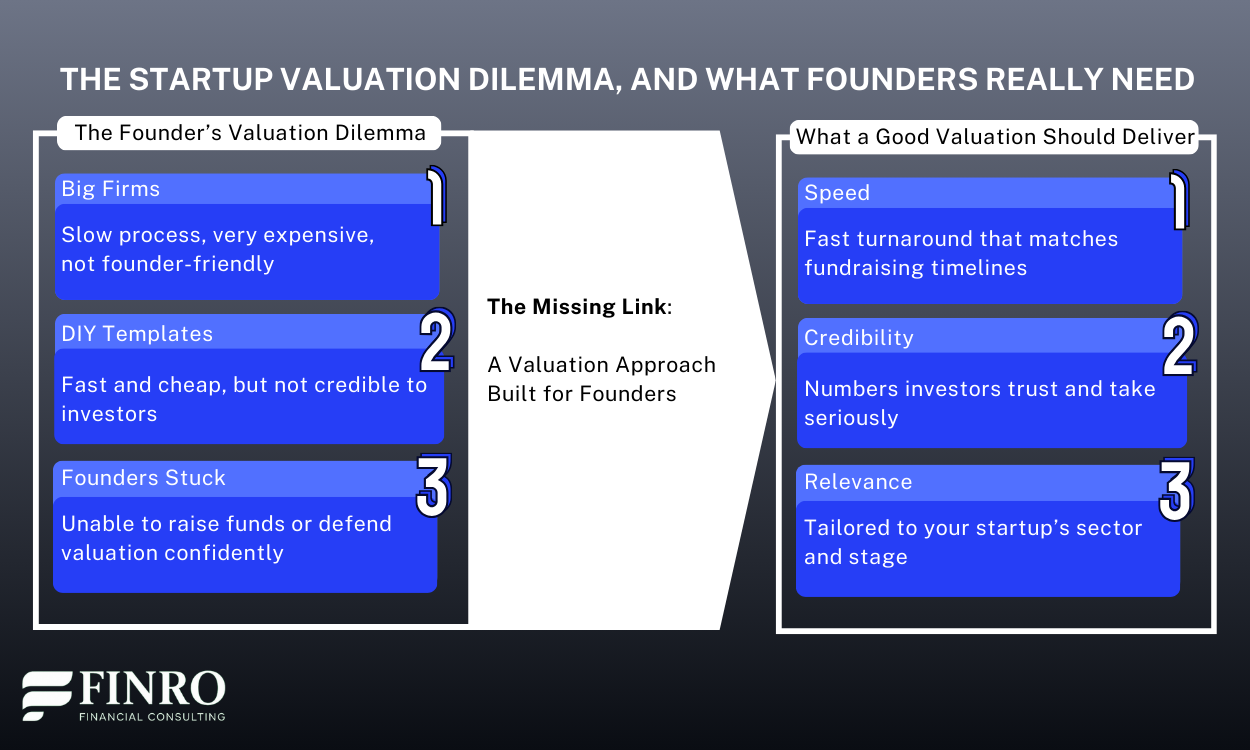

Founders often discover that getting a reliable valuation is not straightforward. Large consulting firms may take six months or more to deliver a report, often charging $35,000–$50,000, which is out of reach for most early-stage startups. At the other extreme, online templates or DIY spreadsheets produce numbers quickly, but these rarely stand up to investor scrutiny.

What founders actually need is a valuation process that balances speed, credibility, and relevance. A valuation must move at the pace of fundraising, use sector-specific benchmarks, and be built in a way that allows founders to confidently explain it to investors.

Specialized firms, such as Finro, are built around these principles. Since 2014, Finro has worked with more than 200 startups across SaaS, AI, Fintech, Cybersecurity, and other sectors, supporting over $1.4 billion in deals. This experience shows that when valuations are both defensible and tailored, they become more than compliance — they become a tool for growth.

TL;DR

Topics covered in this article

- Why Do Startup Valuations Often Go Wrong?

- What Do Founders Really Need in a Valuation Partner?

- Why These Qualities Change the Outcome?

- How These Outcomes Shape Long-Term Growth?

- How Founders Should Approach the Valuation Process?

- Comparing Valuation Approaches

- Choosing the Right Valuation Method

- Conclusion

- Key Takeaways

- Answers to The Most Asked Questions

Why Do Startup Valuations Often Go Wrong?

Startup valuations go wrong for many founders because the process is either oversimplified or disconnected from how investors actually evaluate companies.

Understanding the common pitfalls helps explain why so many startups end up with numbers that either fail to convince investors or create problems in later funding rounds.

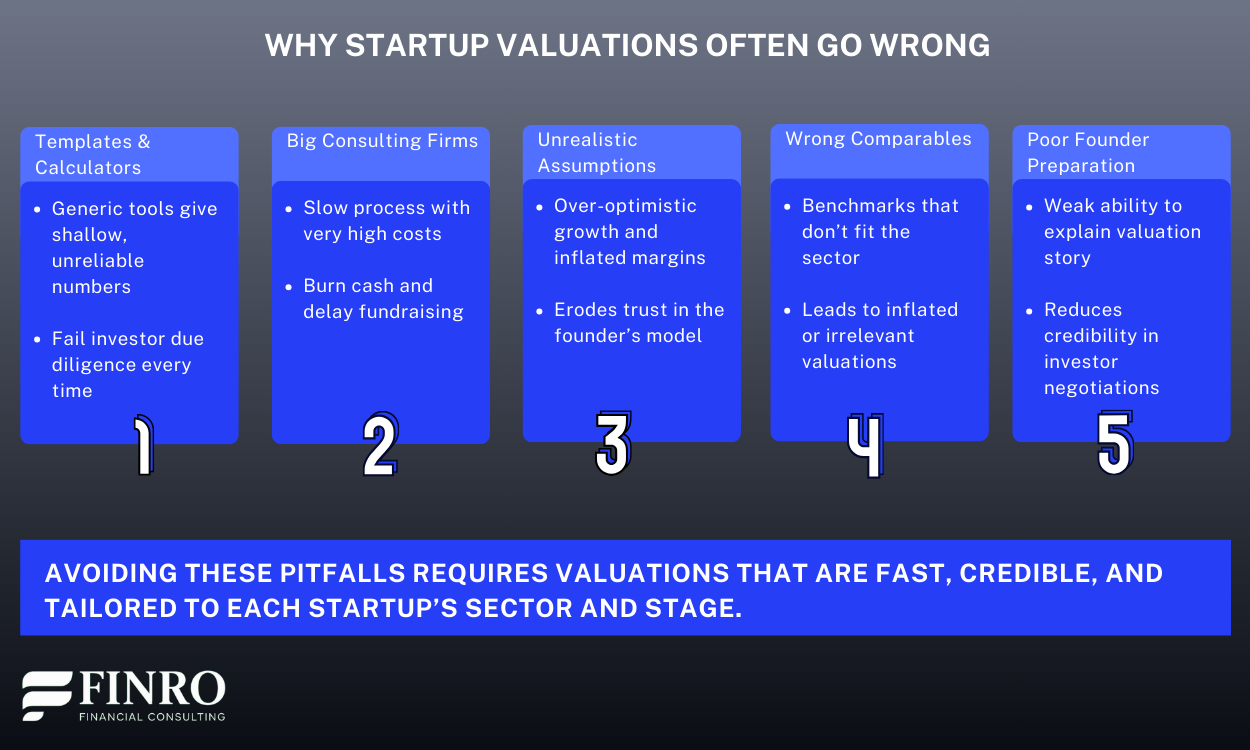

Over-reliance on templates and online calculators

Founders under pressure often turn to quick online calculators or downloadable spreadsheets. While these tools may provide a number instantly, they rarely capture the nuances of a specific business model or sector.

A SaaS startup with recurring revenue, for example, should be valued very differently from a hardware company. Investors know this, which is why valuations that come from generic templates tend to collapse under scrutiny. A better approach is to start from a tailored startup financial model that reflects how the business actually operates.

Reports from large consulting firms

At the other extreme, some founders pursue valuations through large consulting firms. These firms produce extensive, highly detailed reports, but they do so on timelines and budgets that rarely fit the startup context.

A valuation that costs $35,000–$50,000 and takes six months to complete may work for a corporate acquisition, but it can stall a funding round for an early-stage startup. Worse, the frameworks applied are often designed for mature businesses and miss the realities of a fast-growing, pre-revenue or early-revenue startup. Startups benefit more from dedicated startup valuation services that are built with founders in mind.

Unrealistic assumptions in financial models

Another common mistake is presenting projections that don’t match real-world dynamics. Founders sometimes show steep revenue growth starting the same month fundraising begins, or margins that resemble those of established industry leaders.

While optimism is natural in early-stage companies, investors quickly discount valuations built on unrealistic assumptions. This creates a credibility gap, making negotiations harder and eroding trust between founder and investor.

Thinking About Your Next Valuation Step?

Share your stage, context, and objective, and we’ll outline how we would frame the valuation, what assumptions matter, and where investors will focus.

Typical next step: a 15 to 20 minute strategy call.

Lack of sector-specific comparables

Valuations are never built in a vacuum; they depend heavily on relevant comparables. An AI startup focused on infrastructure is not valued the same way as a fintech company in payments or a biotech firm in drug discovery.

Using the wrong benchmarks — or none at all — often results in inflated or irrelevant valuations. Experienced investors will immediately notice when a company is positioned against the wrong peer set, and this weakens the founder’s position in negotiations. Founders can avoid this by referencing Fintech startup valuation multiples or other niche benchmarks Finro publishes.

Weak founder preparation

Even when the numbers themselves are defensible, founders sometimes fail in how they present them. Investors expect founders to understand the logic behind the valuation, the assumptions in their model, and the benchmarks being used.

A founder who cannot clearly explain their valuation risks losing credibility, even if the underlying work is sound. In practice, the ability to defend the valuation is as important as the valuation itself.

Avoiding these pitfalls requires more than a quick calculation or a lengthy report. What founders truly need is a valuation partner who can deliver speed, credibility, and sector relevance in a way that aligns with the realities of startup fundraising.

What Do Founders Really Need in a Valuation Partner?

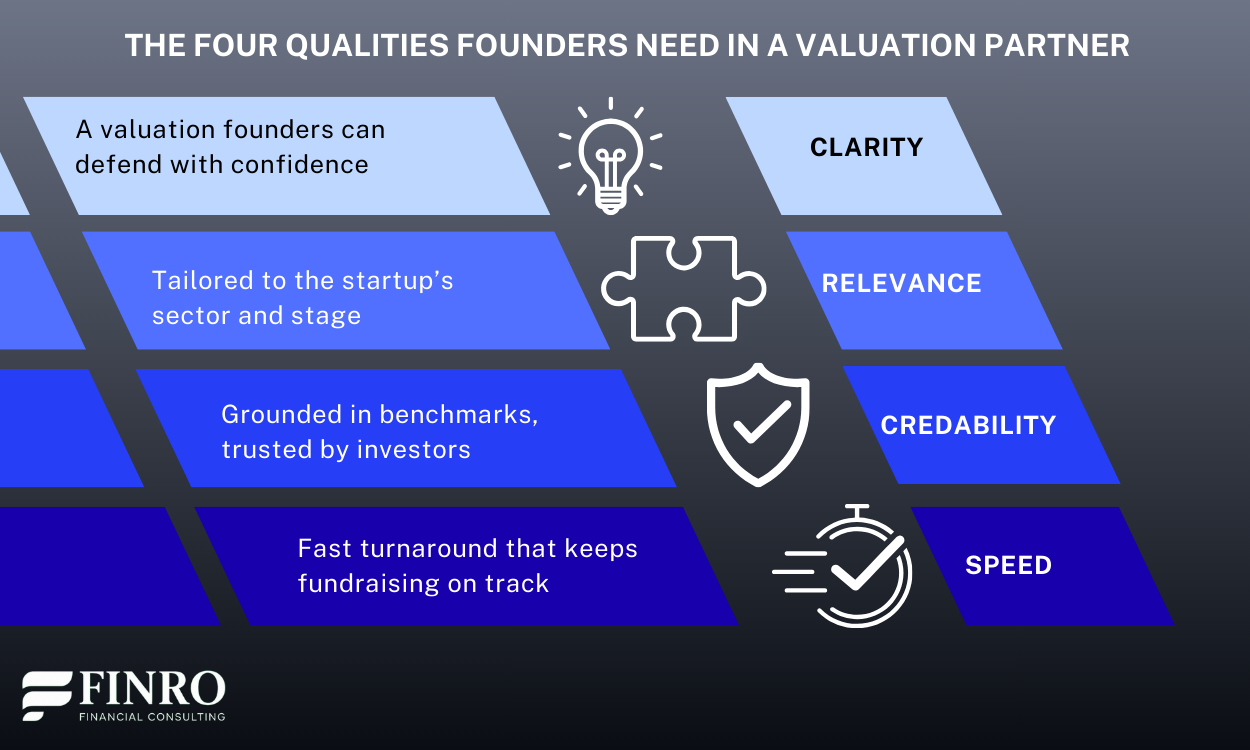

If poor valuations stall fundraising or weaken credibility, the obvious question is what makes a good one. For most founders, the answer lies in finding a valuation partner who understands both the pace of startups and the expectations of investors.

A strong valuation process begins with speed. Startups don’t have the luxury of waiting months for a report while a funding round loses momentum. The right partner can deliver results in weeks, ensuring that valuations move the process forward instead of slowing it down. Yet speed alone is not enough.

A valuation also needs to carry credibility with investors, grounded in accepted methods, sector benchmarks, and assumptions that hold up under due diligence. Numbers that cannot be defended quickly lose value.

Relevance is just as important. Every startup is different, and an AI platform, a SaaS business, or a biotech venture requires different comparables and approaches. Tailoring the valuation to the company’s sector, stage, and model ensures that the number reflects real-world investor expectations rather than generic templates.

Finally, founders need clarity. A valuation only works if it can be explained in the room. Good advisors make sure founders understand the assumptions and benchmarks, making the valuation a tool for both storytelling and compliance.

These qualities explain why founders who avoid common pitfalls are better positioned in fundraising. At Finro, the same principles — speed, credibility, relevance, and clarity — have guided our work with more than 200 startups since 2014.

How Robust Is Your Financial Model?

Before showing your model to investors, it is worth asking a few simple questions.

- Can every revenue assumption be traced to a real acquisition channel or pricing driver?

- Do CAC and retention assumptions reflect realistic scaling dynamics?

- Do margins expand because of operational changes — not just spreadsheet logic?

- Does the hiring plan match the company's ability to acquire and serve customers?

- Can the model clearly explain capital needs and runway under different scenarios?

If any of these questions are difficult to answer, the model may benefit from an external review before investor discussions begin.

See How the Financial Model Review WorksWhy These Qualities Change the Outcome?

The pitfalls we covered earlier explain why so many valuations fail to convince investors, while the four qualities outlined above highlight what founders should look for in a valuation partner. Together, they set a clear contrast between what doesn’t work and what truly moves a fundraising process forward.

When valuations are built with speed, credibility, relevance, and clarity, they serve a dual purpose. On one hand, they meet the technical and financial standards required in due diligence. On the other, they equip founders with a narrative they can confidently explain in investor meetings. This combination reduces friction in negotiations, shortens timelines, and builds trust — all of which directly impact the success of a round.

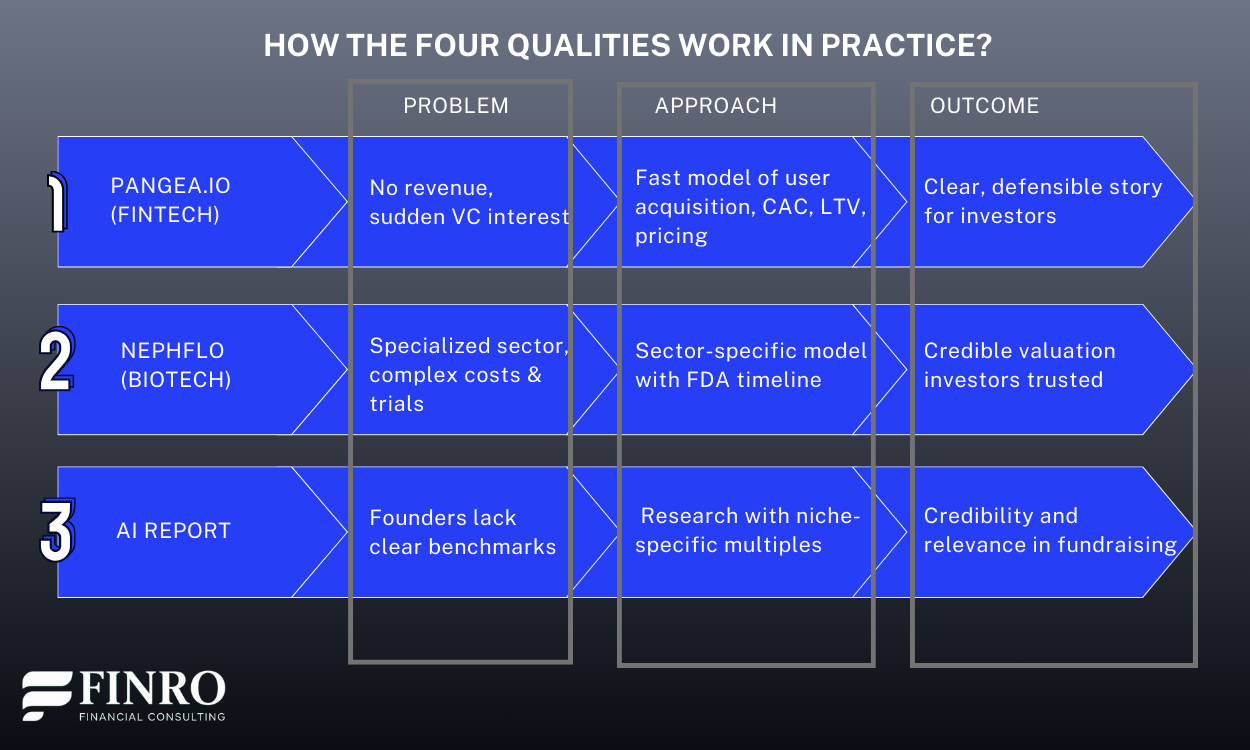

The best proof comes from real-world examples. At Pangea.io, an early-stage fintech startup with zero revenue but sudden VC interest, we quickly turned the founder’s vision into a comprehensive financial model covering transaction volumes, pricing, CAC, LTV, and cash flows. The result was a clear, defensible model that impressed investors and gave the founder confidence in discussions.

For NephFlo, an early-stage biotech venture building an artificial implantable kidney, relevance and credibility were critical. We built a detailed model that accounted for lab equipment, trial costs, FDA timelines, and payroll. Even in a highly specialized domain, the valuation stood up because it reflected the sector’s unique realities.

And in the broader AI sector, our AI Startup Valuation Report provides founders with tailored benchmarks, revenue multiples across niches, and insights into the “AI premium” investors apply. For AI-driven fundraising, this gives both credibility and relevance—key elements that make investor conversations more productive.

These examples illustrate that when valuations are fast, credible, relevant, and clear, they become more than just compliance exercises. They turn into tools for stronger fundraising, smoother negotiations, and greater strategic clarity.

In the next section, we’ll explore how these outcomes not only improve investor conversations today but also set startups on a stronger path for long-term growth.

How These Outcomes Shape Long-Term Growth?

The immediate impact of a strong valuation is noticeable: smoother investor conversations and a more efficient fundraising process. But the benefits don’t stop at closing a round.

The qualities that make a valuation effective, speed, credibility, relevance, and clarity, also shape how a startup grows in the years that follow.

First, they strengthen investor relationships. When valuations are built on defensible assumptions and sector-specific benchmarks, investors feel more confident in the numbers. That trust carries forward into board meetings, reporting cycles, and future rounds, creating a foundation of alignment rather than friction.

Second, they provide founders with a clearer strategic lens.

A valuation grounded in realistic projections forces clarity about growth drivers, costs, and milestones. This isn’t just useful for a pitch deck, it becomes a management tool that helps founders prioritize resources, identify risks, and adjust their trajectory as the company scales.

Finally, strong valuations reduce the risk of painful corrections. Overinflated numbers can lead to down rounds, strained investor relations, and lost credibility in the market.

By contrast, valuations that are credible and tailored set startups on a path where each round builds on the last, preserving momentum and ownership.

In the next section, we’ll look more closely at how founders can approach the valuation process itself — the practical steps that ensure their numbers are both defensible and investor-ready.

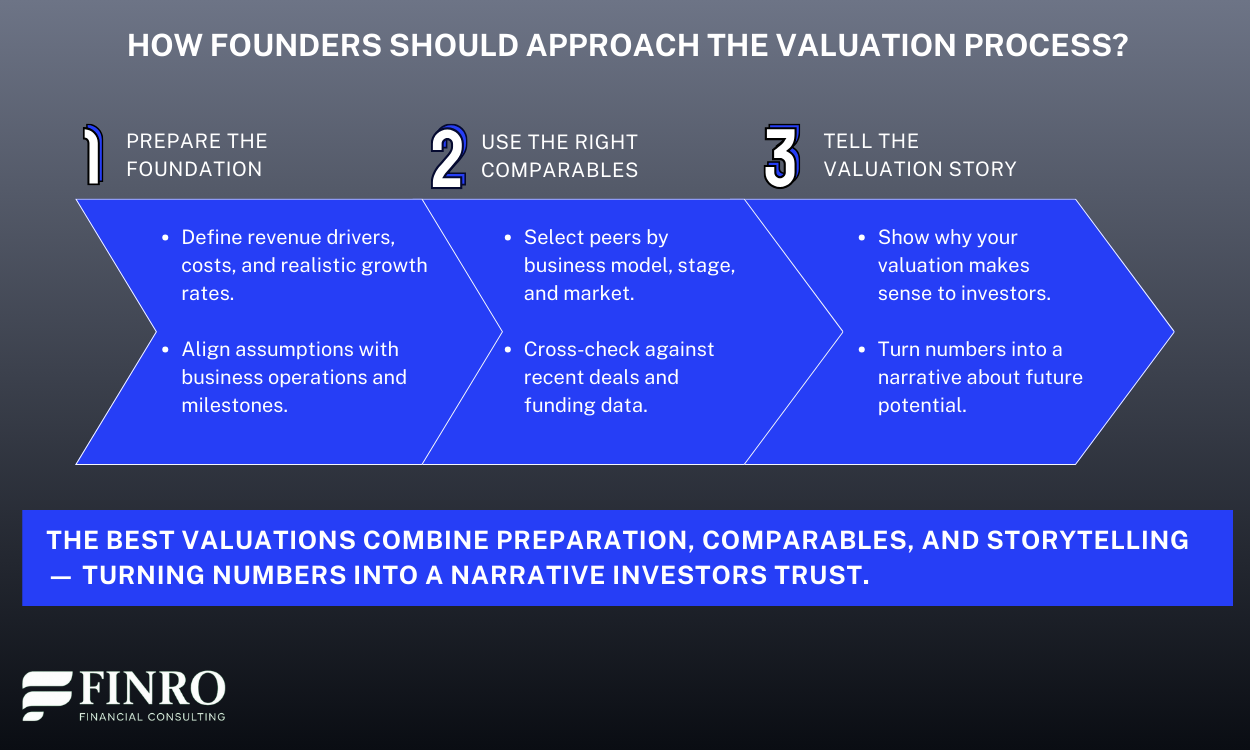

How Founders Should Approach the Valuation Process?

Strong valuations don’t happen by accident. They are the result of a clear process that balances market benchmarks with the specific dynamics of a startup.

For founders, the goal is not just to arrive at a number, but to build a valuation they can defend in front of investors.

The first step is preparation. This means organizing financial data, building a realistic model, and making sure assumptions about growth, costs, and margins reflect how the business actually operates. A model that is both ambitious and grounded becomes the foundation of a credible valuation.

Next comes comparables. Investors rarely assess startups in isolation. They look at sector-specific revenue multiples, recent M&A deals, and funding benchmarks.

Founders who anchor their valuation against the right peer set show they understand their place in the market and avoid the trap of inflated or irrelevant numbers.

Finally, founders should focus on storytelling. A valuation isn’t just a spreadsheet—it’s a narrative about the company’s trajectory.

Explaining why certain benchmarks were chosen, how growth will be achieved, and what milestones lie ahead transforms the valuation from a static figure into a strategic tool.

When approached in this way, the valuation process becomes more than compliance for fundraising. It gives founders clarity about their business and strengthens the story they present to investors.

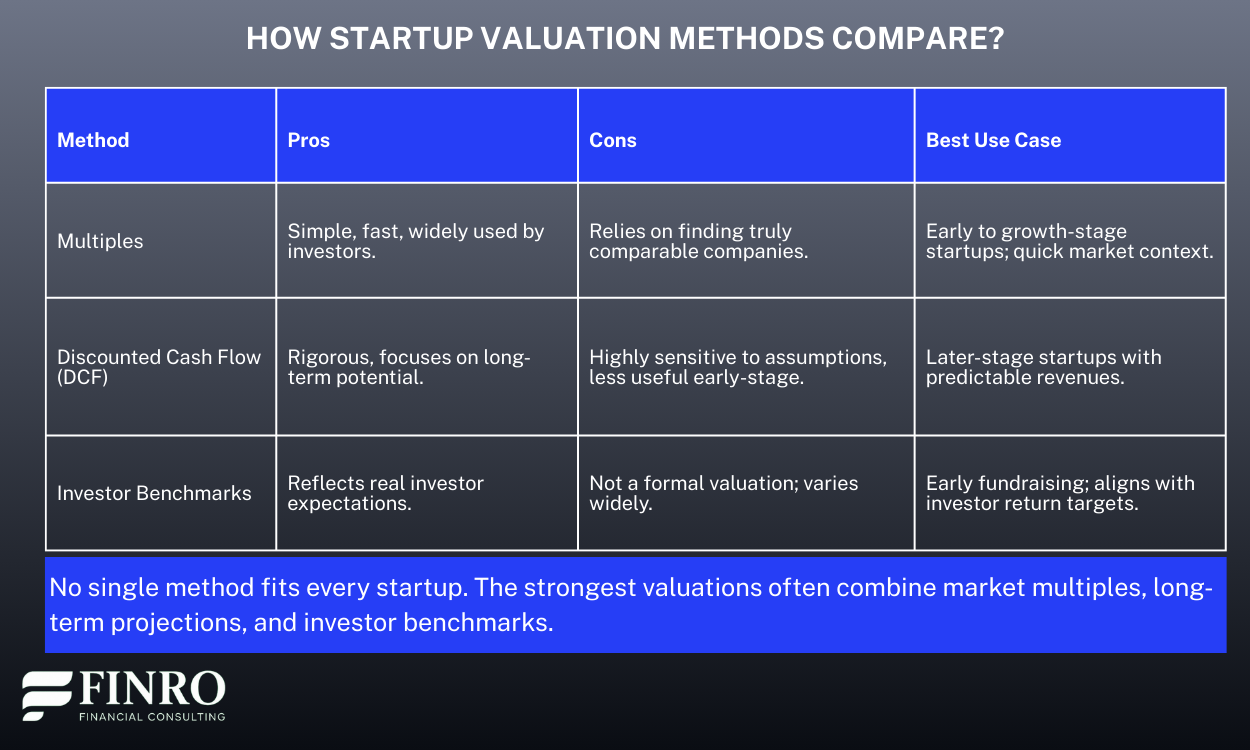

Comparing Valuation Approaches

Founders often ask which valuation method investors prefer. The reality is that no single approach fits every startup. Instead, investors and advisors draw on several methods, each with its strengths and limitations.

Understanding the differences helps founders know which approach is most relevant to their stage and sector.

The most common method is the use of multiples. This approach compares a startup’s metrics — typically revenue or sometimes gross profit — against comparable companies in the same sector. Multiples are straightforward and widely used, but their accuracy depends entirely on choosing the right peer group.

A SaaS startup, for example, may be valued at a revenue multiple, while a fintech platform in payments might rely more on transaction volume or take-rate.

Another method is discounted cash flow (DCF). This projects a startup’s future cash flows and discounts them back to present value. While DCF is conceptually rigorous, it is often less relevant for early-stage companies.

Forecasts are highly uncertain, and even small changes in assumptions can create large swings in the valuation. For later-stage startups with more predictable revenue, however, DCF can provide valuable insight.

Finally, there is the investor benchmark approach. Many investors carry their own rules of thumb — such as typical ownership targets, expected returns, or valuation caps based on stage.

While these are not strictly financial models, they matter in practice because they reflect how investors think about risk and returns. Founders who understand these benchmarks are better equipped to anticipate investor expectations.

Each method has a place.

Multiples provide quick market context, DCF highlights long-term potential, and investor benchmarks reveal the realities of deal-making. Founders who understand all three approaches are better prepared for investor conversations and can present a valuation that is both defensible and aligned with the market.

In the next section, we’ll bring these threads together and look at how founders can choose the right valuation approach for their stage — and why combining methods often creates the strongest outcome.

Choosing the Right Valuation Method

With several approaches available, the key question for founders is which method to use. The answer depends largely on stage, sector, and the story being told to investors.

Early-stage startups typically lean on multiples and investor benchmarks. At this stage, revenues are limited or unpredictable, making discounted cash flow less reliable.

What matters most is showing investors that the valuation is grounded in relevant comparables and consistent with how similar deals are being priced in the market.

Benchmarks also play a role here, since investors often come with clear expectations about ownership and return profiles.

For growth-stage or later-stage startups, discounted cash flow becomes more useful. Once revenues stabilize and costs are more predictable, projecting future cash flows adds credibility.

Multiples still provide valuable context, but investors expect to see the longer-term picture as well. A balanced approach, combining DCF with comparables, often creates the most defensible outcome.

Ultimately, strong valuations rarely rely on a single method. Founders who understand how investors use each approach — and who can reference more than one — are better positioned to defend their numbers.

A blended approach not only strengthens credibility but also shows sophistication in how the founder understands the business.

In the conclusion, we’ll bring everything together — the pitfalls to avoid, the qualities that matter, the methods that work — and show why founders who follow these principles are better prepared for investor conversations.

Conclusion

For founders, valuation is never just about a number. It’s about credibility with investors, confidence in negotiations, and clarity in how the business will grow.

Too often, valuations go wrong because they rely on generic templates, unrealistic assumptions, or benchmarks that don’t fit.

The alternative is straightforward but powerful: build valuations that are fast enough to match fundraising timelines, credible enough to stand up to due diligence, relevant to your sector and stage, and clear enough to explain in the room.

These qualities don’t just improve the odds of closing a round — they shape stronger investor relationships and set the foundation for sustainable growth.

Founders who approach valuation this way are better prepared, better positioned, and ultimately better equipped to tell their story with confidence.

Key Takeaways

Generic templates or inflated assumptions weaken startup valuations.

Strong valuations require speed, credibility, relevance, and clarity.

Real-world cases prove that better valuations lead to stronger fundraising outcomes.

The right method depends on stage, sector, and investor expectations.

Valuations done right build investor trust, strategic clarity, and sustainable growth.

Answers to The Most Asked Questions

-

The best approach combines market multiples, investor benchmarks, and realistic financial models. Founders should tailor methods to their sector, stage, and investor expectations.

-

Valuations often fail because they rely on templates, inflated assumptions, or irrelevant comparables. Investors quickly lose trust when numbers don’t reflect market reality or business fundamentals.

-

Founders defend valuations by understanding benchmarks, building credible financial models, and explaining assumptions clearly. Confidence and transparency turn numbers into a persuasive story investors respect.

-

Early-stage startups typically use multiples and investor benchmarks. DCF is less useful at this stage because future revenues and cash flows are too unpredictable.

-

Strong valuations build investor trust, provide strategic clarity, and avoid down rounds. They create momentum that supports fundraising, strengthens relationships, and protects founder ownership.