Core vs. Applied AI: The Valuation Split That Matters in Q1 2026

The widening gap between Core AI and Applied AI in Q1 2026 reflects the broader dispersion highlighted in Finro’s latest AI valuation multiples analysis, where execution models, not category labels, increasingly determine pricing outcomes.

The market is no longer rewarding “AI exposure” in the abstract. It is rewarding where value accrues and how reliably it compounds, yet most comps sets still struggle to separate those dynamics cleanly across transaction types and segments.

Core versus Applied has become one of the clearest lenses for understanding why similar AI companies now land at very different valuation outcomes. In Q1 2026, the market did not reprice AI in one uniform move. It repriced underwriting certainty, prioritizing durability of revenue, clarity of monetization, and the strength of unit economics behind growth.

Core AI represents the foundation layer: models, infrastructure, orchestration, developer tooling, and data systems that other products rely on. These businesses can earn premiums when they become difficult to replace or sit on critical paths, but they also face faster diffusion, pricing pressure, and higher sensitivity to compute economics.

Applied AI sits closer to the workflow, embedding intelligence into legal, HR, writing, finance operations, customer support, and vertical execution. Multiples tend to hold when the product ties directly to budgets, renews predictably, and expands across adjacent workflows, and compress when the offering is easy to bundle or replicate.

This article uses the Core versus Applied split to show where premiums are still clearing in Q1 2026, where they are compressing, and why execution quality now shapes valuation outcomes more than narrative momentum.

Positioned alongside Finro’s broader AI valuation multiples analysis and AI agents framework, this lens helps clarify how pricing power is consolidating across the AI stack.

-

01AI multiples split harder in Q1 2026. Investors repriced underwriting certainty over headline growth, creating a clearer divide between AI companies with durable economics and companies still relying on scarcity or narrative.

-

02Public, private, and M&A markets are pricing different forms of evidence. Public comps anchor what is defensible, private rounds price scarcity-driven upside, and M&A deals enforce ROI, integration logic, and buyer-specific value.

-

03Core AI premiums survive only when the company becomes infrastructure. Core AI earns premium multiples when it becomes indispensable to the AI stack, improves its cost curve, and creates hard-to-replace technical leverage. Otherwise, multiples compress quickly.

-

04Applied AI holds up when it owns a renewable workflow. Applied AI companies price more consistently when they sell into clear budget owners, support repeatable rollout, create workflow dependence, and show credible expansion motion.

-

05Replaceable or services-heavy AI compresses faster. AI companies lose valuation support when the product is easy to replace, implementation is too services-heavy, gross margins are unclear, or customers do not treat the solution as a recurring operating workflow.

Topics covered in this article +

- Why this split is showing up now

- How founders and investors apply these multiples

- Related AI valuation research and cross-market context

- Why Applied AI tends to price more consistently than Core AI

- Core AI: where premiums survive and where they do not

- Applied AI: where premiums survive and where they do not

- Inside the Core vs. Applied AI Valuation Dataset Q1 2026

- Summary

- Key takeaways

- Answers to the most asked questions

Why this split is showing up now

The Core vs. Applied distinction has existed for years. What changed in Q1 2026 is that investors started using it as a shortcut for one question: where does underwriting risk actually sit.

Core AI carries structural uncertainty that is hard to hand-wave away. Capability diffuses quickly, open alternatives keep improving, and price competition tends to show up faster than teams expect.

Even when a Core company is genuinely ahead, buyers often treat performance as a moving target and push for better economics each renewal cycle. That makes Core outcomes increasingly hinge on defensible distribution, a clear billable unit, and proof that margins improve as usage scales.

Applied AI has its own risks, but they are easier to diligence. Buyers can point to a workflow, a budget line, and measurable impact.

When an Applied product is embedded in a recurring process, renewals become operational rather than discretionary. That reduces the number of “ifs” in the story, which is exactly what the market has been repricing.

This is also where the public, private, and M&A lenses start to align. Public comps tend to punish weak gross margin trajectory and unclear unit economics. Private rounds can still pay for upside, but only when scarcity and category leadership feel credible.

M&A is the strictest filter because it has to clear a buyer’s ROI model and integration reality, which is why acquisition pricing tends to be more grounded. When you map companies to Core or Applied, you can usually predict which of these filters they will clear most easily.

The practical takeaway is that “Core vs. Applied” is not a tech taxonomy. It is an underwriting taxonomy. It explains why two companies can both be “AI companies,” both be growing quickly, and still see very different valuation outcomes.

These structural differences are reflected across Finro’s Q1 2026 AI valuation dataset, where multiples diverge meaningfully between infrastructure, agents, and applied AI workflows.

AI valuation premiums survive for different reasons

Core AI and Applied AI are not priced on the same evidence. Core AI earns premiums when it becomes infrastructure. Applied AI earns premiums when it owns repeatable, renewable workflows with clear budget ownership.

Core AI

Infrastructure logicThe company becomes a hard-to-replace AI stack dependency with platform pull, developer adoption, improving unit economics, and durable technical advantage.

Model differentiation fades, compute costs stay structurally heavy, switching costs remain low, or distribution depends on temporary scarcity rather than embedded demand.

LLM vendors, infrastructure, data intelligence, search, computer vision, robotics, and developer tooling.

Applied AI

Workflow logicThe product owns a renewable operating workflow, sells into clear budgets, rolls out repeatably, expands inside accounts, and reduces measurable work or cost.

The product looks like a feature, requires heavy services, has unclear renewal behavior, or can be bundled into an incumbent software suite.

HealthTech, FinTech, LegalTech, HRTech, PropTech, productivity tools, marketing technology, sales, and customer operations.

Valuation takeaway: Core AI prices on infrastructure indispensability and improving cost curves. Applied AI prices on workflow ownership, renewability, and expansion quality.

Need the full benchmark? Download the AI valuation dataset with 575 companies across 15 AI segments, including public, private, and M&A valuation multiples.

Download datasetHow do founders and investors apply these multiples?

Valuation multiples are useful, but only after the benchmark is translated into company-specific logic. A market multiple can show how comparable companies are being priced, but it does not explain where a specific company should sit relative to that market.

For founders, the practical use is to test whether the valuation story is supported by revenue quality, growth efficiency, retention, margin profile, and market positioning. For investors, the same data helps pressure-test assumptions, compare opportunities, and separate durable fundamentals from temporary market narrative.

At Finro, these datasets are used in valuation work for fundraising, M&A, investor review, and strategic planning. The objective is to connect market evidence with the company’s actual business model, so the valuation is easier to explain when it is challenged.

What’s Driving the Valuation Gap in AI?

The most important AI valuation signal right now is not the average multiple. It is how aggressively the market separates the same story into very different outcomes.

Based on an analysis of ~580 AI companies across public comps, private rounds, and M&A, three valuation signals show up clearly. Public comps define the reference range for AI exposure, running roughly 2.0x to 41.0x EV/Revenue, and that sets the bar for what a premium needs to earn.

Private rounds express the upside case when investors believe an asset is scarce and can compound into category leadership, which is why private pricing concentrates higher at roughly 10.5x to 37.3x. M&A is the most pragmatic filter because it has to clear a buyer’s ROI model and integration reality, so deals tend to land in a more grounded 2.3x to 26.8x range.

Taken together, those ranges explain the market signal better than any single “AI multiple.” Public markets anchor what is defensible, private markets pay for scarcity-driven upside, and M&A enforces what is actually monetizable.

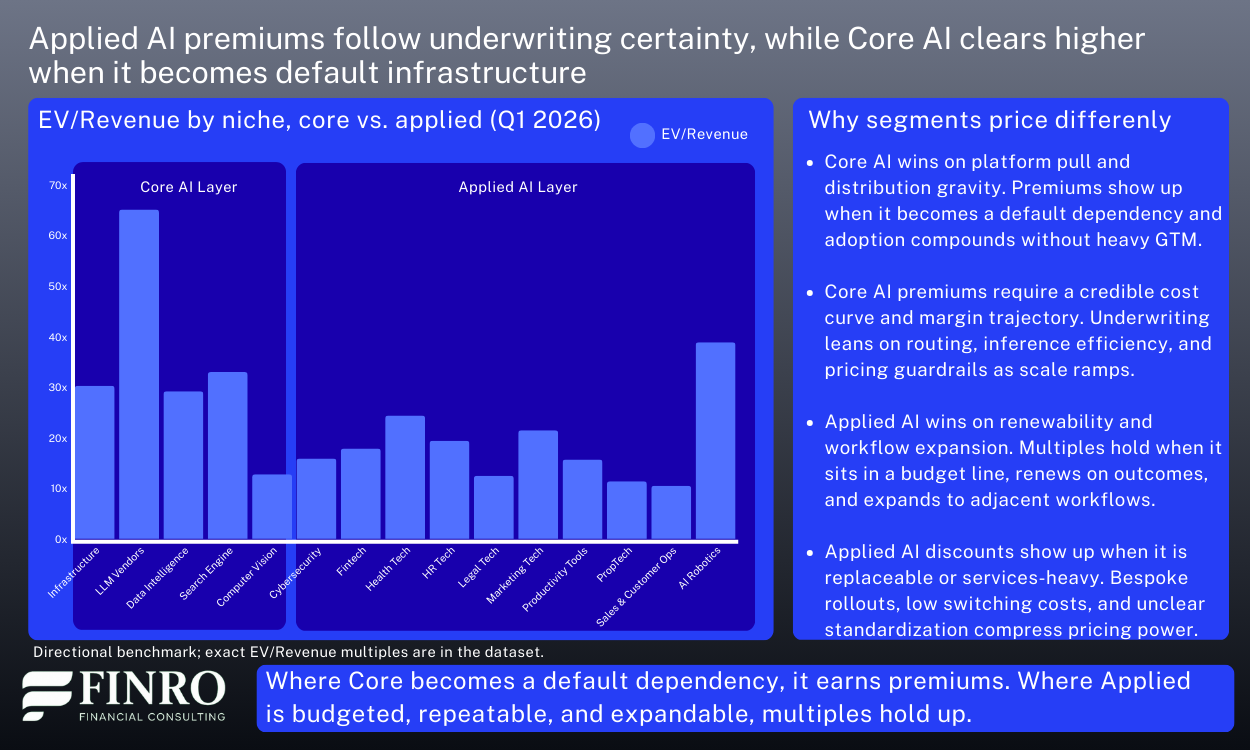

What determines which range a company tends to clear is not the word “AI.” It is where the company sits in the stack. In practice, most of the separation becomes legible once you split the market into two functional layers: core and applied.

Core AI sells the rails, meaning models, infrastructure, and developer tooling. Applied AI sells outcomes inside workflows, such as legal, HR, writing, finance ops, and vertical execution.

That split explains most of the dispersion. Core AI can command premium pricing when it becomes picks-and-shovels infrastructure other companies must build on. When an infrastructure asset becomes a workflow primitive with expansion pull, private pricing can clear premium territory even before margins fully mature, because underwriting is about platform leverage and durability, not near-term profitability.

Applied AI is where multiples separate into clearer tiers. Enterprise workflow leaders still earn strong pricing power when the product ties to a budget line, renews predictably, and expands across adjacent workflows. The long tail prices very differently when the product is easier to replace, harder to standardize, or effectively sold as a feature.

Net, “AI multiples” are not one benchmark. Valuations are being set by where the company sits in the stack, how scarce that position is, and how clearly revenue translates into durable economics.

Core AI: where premiums survive and where they don’t?

The earlier sections set the lens. Core AI is where repricing is most unforgiving, because the product sits closer to compute economics, fast capability diffusion, and procurement pressure.

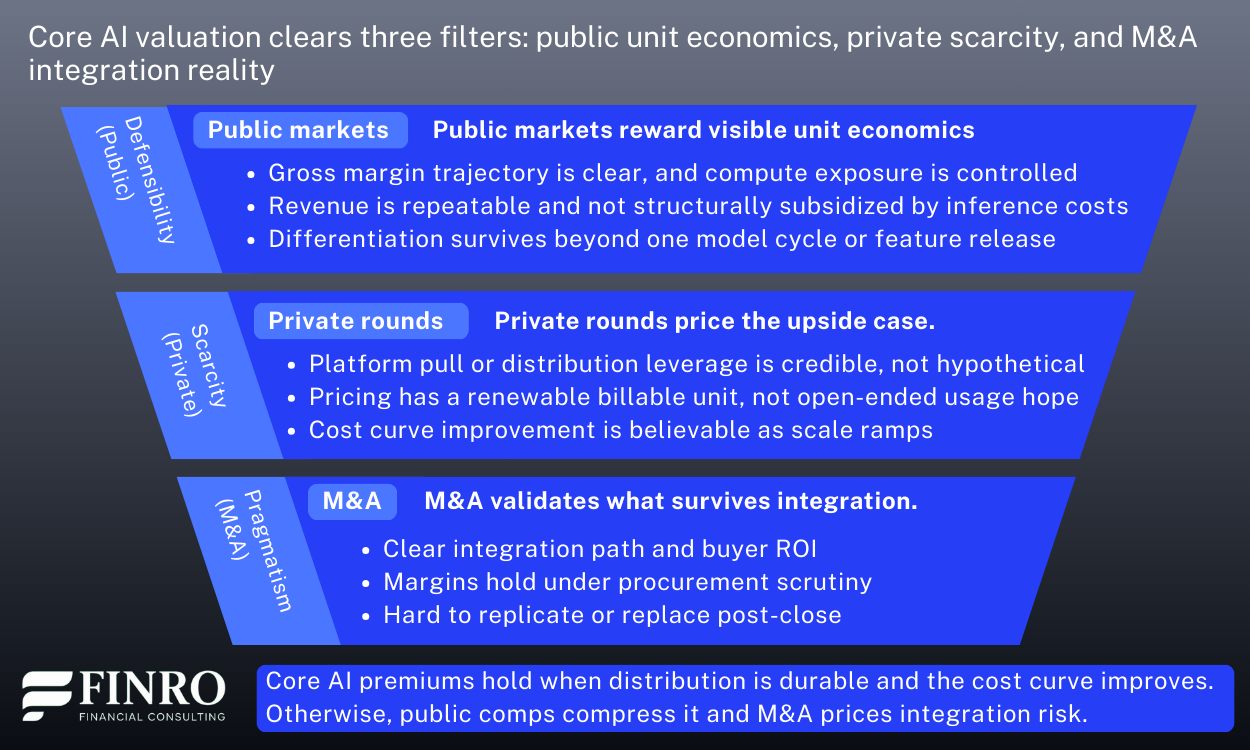

Premiums still clear in Q1 2026, but only when a company passes three tests at once: defensibility in public markets, scarcity-driven upside in private rounds, and pragmatism in M&A.

Public markets reward visible unit economics. In Core AI, “better models” is not the value proposition investors pay for. What holds up is margin trajectory, controlled compute exposure, and revenue that is repeatable rather than structurally subsidized.

Private rounds still pay for scarcity, but it has to look structural. That is why LLM Vendors sit at the top of the Core layer in Q1 2026, with private EV/Revenue averaging ~79.7x and an overall category average of ~65.2x. The premium is underwriting platform pull and distribution leverage, not current profitability.

M&A is the reality check. Buyers still pay for strategic Core assets, but pricing has to clear integration and ROI constraints. You see that gap in LLM Vendors, where M&A averages ~54.8x versus private ~79.7x, and in Infrastructure, where pricing is strong but more grounded (~33.2x private, ~26.4x M&A, ~30.3x overall). Segments that are easier to bundle or replicate compress faster; for example, Computer Vision clears at ~12.8x overall in Q1 2026 (~10.1x public, ~11.9x M&A).

Net, Core AI premiums survive when the product becomes a dependency, and the cost curve is credibly improving. They compress when differentiation relies on the next release cycle, switching costs are low, or compute economics remain the hidden subsidy.

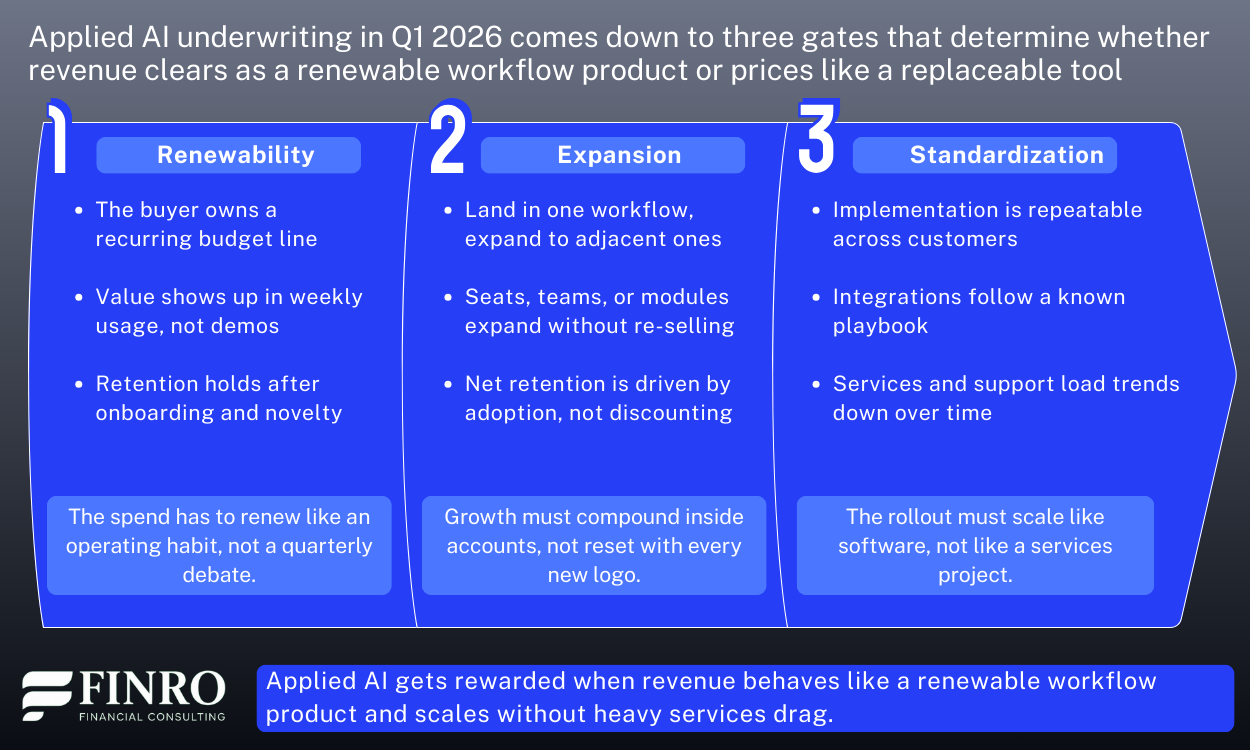

Applied AI: where premiums survive and where they don’t?

Up to here, the pattern is clear. “Core vs. applied” is not a taxonomy exercise, it is the fastest way to explain why some valuation outcomes stay intact while others get marked down. With that lens in place, Applied AI is the part of the stack where pricing looks more explainable, but also more ruthless about what is actually selling.

In Q1 2026, Applied AI does not earn a premium for being impressive. It earns a premium for being renewable. The market is rewarding products that show up as a line item, get used inside a recurring process, and expand without turning every deployment into a services project.

Public comps tend to keep Applied pricing honest. When an offering looks like a feature that can be bundled into an existing suite, or when revenue quality depends on heavy implementation, public multiples compress quickly. When the product behaves like software that renews on habit and expands on usage, the floor is materially higher.

Private rounds are where Applied leaders still clear strong outcomes. The premium shows up most consistently in enterprise workflows where ROI can be defended, procurement is repeatable, and expansion has a clear path. That is why Legal and HR leaders can still carry premium marks, with examples like Harvey around ~80x and Rippling around ~30x, while many “AI-enabled” point solutions cluster much closer to the market’s baseline.

M&A is where the market draws the hardest boundary. Strategic buyers will pay for Applied assets that already own workflow adoption and can be integrated cleanly, but they discount anything that looks like it will be hard to standardize post-close. Even within Legal, you see more grounded outcomes for mature platforms like Icertis at ~14x and Ironclad around ~23x, reflecting how quickly pricing snaps back to integration reality.

Net, Applied AI premiums survive when the product is embedded, renewal is the default, and expansion is mechanical. They compress when the product is easy to swap, easy to bundle, or still relies on bespoke delivery to make the numbers work.

Inside the Core vs. Applied AI Valuation Dataset (Q1 2026)

If the Core vs. Applied split feels sharper in Q1 2026, it reflects the same dispersion highlighted in Finro’s broader AI valuation multiples analysis, where execution models increasingly drive pricing outcomes. The market is no longer rewarding “AI exposure” in the abstract. It is rewarding where value accrues and how reliably it compounds.

Finro’s Q1 2026 AI Valuation Multiples dataset is built to make the split benchmarkable. It covers public comps, private rounds, and M&A across the AI stack, fully tagged by segment so you can compare Core versus Applied on a like-for-like basis and understand which signals are anchoring outcomes.

You can use it to triangulate three things quickly. What the public market treats as defensible. What private rounds are still willing to pay for when scarcity looks real. And what pricing actually clears when a buyer has to underwrite ROI and integration.

The file includes 575 companies across 15 AI segments, with multiples such as EV/Revenue and EV/Funding, plus summary views by segment and transaction type, and dedicated cuts for Core vs. Applied and agentic exposure. It is designed to be pivot-ready so you can build a comps view, pressure test a valuation range, or sanity check a round narrative in minutes.

For the broader market context behind these benchmarks, see Finro’s full AI valuation multiples analysis.

Need the full Core vs. Applied AI valuation dataset?

Download the Excel dataset behind this analysis, covering AI valuation benchmarks across public comps, private rounds, and M&A transactions.

Summary

Core vs. Applied is not a semantic distinction in Q1 2026. It is the cleanest way to explain why similar AI stories land at very different valuation outcomes.

Core AI can still clear premium revenue multiples, but the bar is structural. Premiums hold when the product becomes a dependency in the stack, distribution is durable, and the cost curve is credibly improving. Where differentiation relies on the next release cycle, switching costs are low, or compute remains the hidden subsidy, public comps compress quickly and M&A prices the asset through integration and ROI risk.

Applied AI behaves differently because underwriting is closer to the budget. Multiples hold when revenue renews like an operating habit, expands inside accounts without constant re-selling, and the rollout scales like software rather than services.

When value is harder to standardize, deployments stay bespoke, or the product is easy to bundle, pricing compresses into the “replaceable tool” tier even if the product looks impressive.

Taken together, the takeaway is practical. In Q1 2026, valuation outcomes are being set less by the label “AI” and more by where the company sits in the stack and how predictably revenue converts into durable economics.

If the business reads as a dependency with an improving cost curve, the market pays up. If it reads as a feature with fragile margins or fragile renewals, the market reprices it fast.

- 1 Q1 2026 repriced underwriting certainty, not AI exposure. Revenue quality, margin trajectory, renewability, and monetization clarity now explain valuation outcomes better than the broad label “AI.”

- 2 Public, private, and M&A markets apply different valuation filters. Public comps anchor what is defensible, private rounds price scarcity-driven upside, and M&A deals enforce ROI, integration logic, and buyer-specific value.

- 3 Core AI premiums survive only when the product becomes infrastructure. Core AI companies earn stronger multiples when they become hard-to-replace dependencies with durable distribution, improving compute economics, and repeatable revenue.

- 4 Applied AI prices more consistently when it owns a renewable workflow. Applied AI companies hold stronger valuation support when they sell into clear budgets, renew predictably, expand inside accounts, and scale without heavy services drag.

- 5 Feature-like or services-heavy AI compresses faster. Multiples weaken when the product is easy to replace, easy to bundle into an incumbent suite, hard to standardize, or dependent on bespoke implementation to create value.

- 6 AI valuation benchmarks need stack position and transaction context. A useful AI multiple depends on whether the company is Core or Applied, how defensible its revenue is, and whether the benchmark comes from public comps, private rounds, or M&A deals.