AI Startup Valuation Services: How Investors Evaluate Companies in 2026

AI startup valuation in 2026 is no longer driven by growth narratives alone.

Investors are trying to determine what kind of business they are looking at, how resilient its revenue engine is, how cost exposure evolves as it scales, and how much execution risk sits between today’s traction and long-term durability.

Two AI startups with identical revenue can land in very different valuation ranges. One may show compounding usage with improving unit economics and infrastructure leverage. The other may depend on unstable pricing, heavy compute exposure, or customer concentration risk.

The difference is rarely presentation. It is structure.

This article explains how investors actually evaluate AI startups in 2026 and how structured valuation support helps founders translate economic reality into a defensible valuation range.

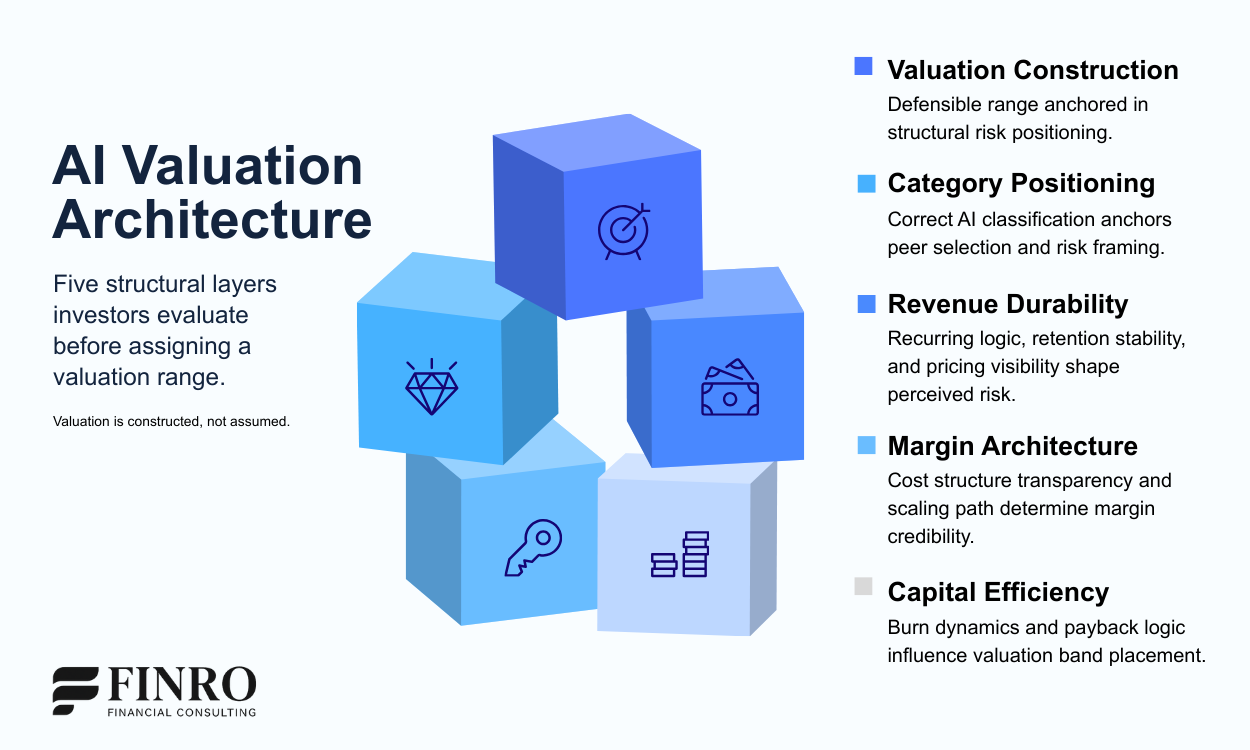

AI startup valuation is not driven by headline multiples. Investors construct valuation ranges after evaluating structural risk across category positioning, revenue durability, margin architecture, and capital efficiency. A defensible valuation is built through alignment with comparable risk profiles, not narrative momentum.

Topics covered in this article +

- What AI startup valuation actually means

- How investors evaluate AI companies in 2026

- Revenue model quality

- Margin architecture and infrastructure exposure

- Capital efficiency and burn structure

- Competitive defensibility

- Where AI founders commonly misalign with investor expectations

- How structured valuation support changes the conversation

- When AI companies engage a valuation advisor

- How Finro approaches AI startup valuation

- Business model and category mapping

- Revenue durability and unit economics review

- Margin architecture and cost structure analysis

- Capital efficiency and risk calibration

- Comparable alignment and valuation range construction

- Translating structure into investor confidence

- Key takeaways

- Related startup valuation guides and advisory services

- Answers to the most asked questions

What AI Startup Valuation Actually Means

AI startup valuation is the structured assessment of enterprise value based on economic quality, risk exposure, and market positioning.

It is not a surface-level pricing exercise. It is an analysis of how the business behaves under scale.

At its core, valuation answers a simple but difficult question:

How predictable is this company’s future cash-generating capacity, and what risks sit between today’s performance and that future?

In AI startups, that question becomes more complex because revenue often scales through usage, infrastructure exposure, model dependencies, and evolving cost structures. Growth alone does not explain whether the business becomes stronger or more fragile as it expands.

Investors, therefore, do not start with valuation. They start with structure.

They examine:

How revenue is generated and retained

How margins evolve as usage increases

How compute, infrastructure, or third-party dependencies affect cost stability

How customer concentration or pricing sensitivity might shift over time

How capital is deployed relative to growth efficiency

Only after those structural dynamics are understood does a valuation range begin to make sense.

AI companies vary widely in how these elements behave. Infrastructure providers operate under different capital intensity than vertical AI SaaS businesses. Agentic platforms introduce different execution risk than workflow automation tools. Even companies with similar revenue levels can carry fundamentally different economic profiles.

Valuation is therefore less about matching categories and more about interpreting behavior.

When founders approach valuation as a structural translation exercise rather than a headline comparison, conversations with investors tend to become more grounded, more analytical, and more productive.

That is where structured valuation support adds value: clarifying how the business truly works before attaching a price to it.

What Valuation Translates Into a Defensible Range

AI valuation is not a single number. It is a structured view of economics, risk, and repeatability.

Revenue behavior

How revenue is generated, retained, and expanded inside real workflows.

Margin structure

What actually drives gross margin and how it moves as usage scales.

Risk surface

Concentration, dependency, compliance, and execution risks that change pricing.

Capital efficiency

How efficiently growth converts into durable enterprise value over time.

How Investors Evaluate AI Companies in 2026

AI valuation discussions rarely begin with price. They begin with a diagnosis.

Investors first try to understand what type of AI company they are evaluating and how its economics behave under scale. In 2026, capital is more selective, and the tolerance for narrative-driven assumptions has narrowed. The focus has shifted from excitement to structural durability.

Several evaluation layers consistently shape valuation conversations.

Revenue Model Quality

Investors examine how revenue is generated and whether it compounds.

Is growth driven by usage expansion inside existing accounts, or constant customer acquisition?

Does pricing reflect value creation, or is it vulnerable to compression?

Is revenue contractual, consumption-based, or project-driven?

AI companies built around embedded workflows and expanding usage often present more durable revenue patterns than those relying on one-off deployments or thin integrations. The difference directly affects how confidently future cash generation can be projected.

Margin Architecture and Infrastructure Exposure

Margin behavior in AI businesses is rarely static.

Compute costs, model dependencies, licensing agreements, and third-party APIs can materially shape gross margin over time. Investors evaluate whether margin improves with scale or remains exposed to infrastructure constraints.

An AI company with clear cost layering and improving unit economics is interpreted differently from one where scaling usage increases cost volatility.

Capital Efficiency and Burn Structure

Growth financed through disproportionate capital consumption signals fragility.

Investors look at the startup financial model for burn multiple, CAC payback, and the relationship between capital deployed and revenue durability. Efficient growth suggests control. Capital intensity without margin progression suggests execution risk.

In tighter funding environments, this dimension has become more influential than headline growth rates.

Competitive Defensibility

AI markets move quickly. Investors assess how defensible the company’s position is within its category.

Is there proprietary data creating advantage?

Are workflows deeply integrated?

Does switching cost increase over time?

Is the company dependent on upstream model providers without differentiation?

Defensibility influences both upside and downside scenarios, which directly affects valuation range interpretation.

How Investors Move From Analysis to a Valuation Range

Valuation is the output. The range forms after investors understand how risk, durability, and scalability behave inside the model.

Category clarity

What type of AI business is this, and why does that category deserve the benchmark?

Revenue durability

Recurring behavior, retention logic, contract visibility, and how revenue compounds.

Margin architecture

COGS reality, inference costs, delivery model, and the path to scalable margins.

Capital efficiency

Burn, payback, sales efficiency, and whether growth improves or consumes efficiency.

Risk band positioning

The company is placed against comparable risk profiles, then converted into a defensible valuation range.

Where AI Founders Commonly Misalign With Investor Expectations

Most valuation friction does not come from disagreement about growth. It comes from structural blind spots.

Founders often approach valuation discussions believing that strong traction or rapid expansion should anchor pricing. Investors, however, are testing whether that growth reflects durable economics or temporary momentum.

Growth alone does not explain valuation. Investors want to understand why growth occurs and whether it strengthens or weakens as scale increases. If usage expansion drives revenue but inference costs rise proportionally, margin structure becomes more important than top-line acceleration. If customer acquisition accelerates but retention remains uncertain, the valuation range reflects that fragility.

Growth is necessary. Structure determines how it is priced.

A second common misalignment appears in positioning. Infrastructure providers, vertical AI applications, agentic platforms, and embedded workflow tools operate under different economic profiles. Benchmarking against companies that look similar on the surface but behave differently underneath weakens credibility quickly. Investors detect category mismatches, and valuation expectations adjust accordingly.

Finally, scenario logic and capital efficiency often receive less attention than they deserve. Single-forecast financial models can signal confidence to founders but uncertainty to investors. Investors assume variability. They test downside exposure and execution sensitivity. Burn rate, CAC payback, compute exposure, and scaling mechanics influence perceived risk as much as revenue velocity.

These differences do not mean founders misunderstand their businesses. They reflect differences in perspective.

Founders see opportunity.

Investors price risk.

Valuation advisory work exists to bridge that gap.

How Structured Valuation Support Changes the Conversation

Valuation conversations tend to shift the moment structure replaces narrative.

When founders approach investor discussions with a high-level growth story, the dialogue often revolves around projections and market potential. When they approach with a structured valuation framework, the discussion moves toward risk calibration, comparability, and defensibility.

That shift matters.

Structured valuation support does not simply produce a number. It clarifies:

what category the company truly belongs to

how revenue durability behaves under scrutiny

how margin architecture scales over time

how capital efficiency influences perceived risk

where the company realistically sits within a valuation band

Instead of debating headline multiples, the conversation becomes anchored in drivers.

Instead of reacting to investor pushback, founders can anticipate it.

Instead of negotiating around a single valuation target, they can explain a defensible range and the logic behind it.

In practice, this changes the dynamic of fundraising and strategic discussions. Investors tend to respond differently when risk is mapped explicitly rather than implied. A well-structured valuation approach signals maturity, discipline, and awareness of market positioning.

It also reduces dispersion. When comparables are carefully selected and assumptions are transparent, valuation expectations narrow. That does not guarantee a higher price. It increases the probability of a credible one.

For AI startups in particular, where business models evolve quickly and economic profiles vary widely across categories, structured valuation support often prevents misalignment before it appears.

The objective is not to inflate valuation. It is to align it with how the market actually prices risk.

When AI Companies Engage a Valuation Advisor

Most AI companies do not need a valuation consultant at incorporation.

They need one when the stakes of interpretation increase.

A valuation becomes relevant when capital allocation, ownership structure, or transaction dynamics start to depend on how risk is framed.

Across AI and tech engagements, advisory support typically enters at one of four inflection points.

1. Preparing for a Fundraising Round

Once a company moves beyond early experimentation and begins structured fundraising, valuation conversations shift from narrative to comparability.

Investors begin asking:

How does this business fit within a defined AI category?

What revenue durability justifies this range?

How do margin assumptions compare to peers?

Where does this sit within risk bands for this stage?

At this point, valuation is no longer theoretical.

It becomes part of negotiation structure.

2. Approaching a Strategic Transaction or M&A Process

In acquisition discussions, the conversation changes again.

Strategic buyers evaluate:

Integration complexity

Margin visibility

Revenue concentration

Regulatory exposure

Capital intensity

Here, valuation is shaped less by growth story and more by risk containment.

A structured approach ensures the company is positioned within the correct strategic peer set rather than benchmarked against mismatched comparables.

3. Secondary Transactions or Internal Equity Decisions

As cap tables become more complex, valuation influences:

Option pricing

Secondary share sales

Founder liquidity events

Internal ownership restructuring

A defensible valuation framework protects both governance and credibility.

4. Investor Disputes Around Assumptions

Sometimes the trigger is not a transaction but tension.

An investor challenges:

CAC payback assumptions

Margin trajectory

Retention durability

Capital efficiency

When discussions center on disagreement about mechanics rather than vision, a structured valuation process reframes the debate.

It shifts the conversation from opinion to calibrated analysis.

The Underlying Pattern

In each of these scenarios, valuation is not about generating a number.

It is about:

Defining category accurately

Mapping revenue durability

Stress-testing margin structure

Aligning risk positioning

Translating model mechanics into investor language

That translation layer is where advisory work adds value.

How Finro Approaches AI Startup Valuation

AI valuation cannot be reduced to a single method or a mechanical multiple selection.

The starting point is diagnostic, not arithmetic.

Across engagements, the work typically moves through five structured layers.

1. Business Model and Category Mapping

Every valuation begins with classification.

In AI markets, category confusion is common. Companies frequently describe themselves as infrastructure, platform, or agentic when their economic profile behaves differently under scrutiny.

Before any numerical work begins, the underlying business logic must be mapped:

What is the core economic engine?

Where does value accrue in the stack?

Is the company model-dependent, workflow-embedded, or service-augmented?

Does pricing reflect product leverage or human intensity?

Misclassification is one of the most common sources of valuation distortion. A vertical AI workflow company will not be evaluated the same way as a developer tooling business, even if both describe themselves as “AI platforms.”

Only once the company is positioned within the correct structural category can peer alignment begin.

2. Revenue Durability and Unit Economics Review

Revenue growth alone does not anchor valuation.

Investors evaluate not just how fast revenue grows, but how stable and repeatable it is under pressure. Early-stage AI businesses often show strong expansion metrics but lack visibility into how durable that expansion is across cohorts.

This stage examines the structural reliability of revenue:

Recurring behavior versus transactional exposure

Retention logic and cohort stability

Pricing architecture and elasticity

Contract visibility and renewal patterns

Contribution margins and payback mechanics

The objective is not to validate projections. It is to understand how revenue behaves when stressed.

Durability, not acceleration, often determines where a company sits within a valuation band.

3. Margin Architecture and Cost Structure Analysis

AI businesses differ materially in cost composition.

Two companies with identical revenue can carry very different margin trajectories depending on compute intensity, inference costs, infrastructure dependency, or human intervention requirements.

Rather than modeling a single gross margin assumption, margin architecture is decomposed into structural drivers:

Model hosting and compute costs

Third-party infrastructure exposure

Data acquisition and processing overhead

Customer support and service intensity

Regulatory or compliance burden

This separation clarifies whether margin expansion is realistic, gradual, or structurally capped.

Investors tend to discount valuation when margin logic is opaque. Clear cost mapping reduces that uncertainty.

4. Capital Efficiency and Risk Calibration

Capital efficiency influences perceived risk more than headline growth.

High-growth AI companies that require persistent capital injections are evaluated differently from those demonstrating improving operating leverage.

This stage connects operational metrics to capital structure:

Burn rate relative to growth

Customer acquisition efficiency

Payback periods and scaling dynamics

Funding runway and dependency

Sensitivity to macro capital conditions

The analysis does not aim to minimize risk. It aims to quantify it.

Understanding how capital intensity evolves over time allows valuation positioning within the appropriate risk band.

5. Comparable Alignment and Valuation Range Construction

Only after the structural layers are mapped does valuation range construction begin.

Comparable selection is not a database exercise. It is a filtering process guided by economic similarity rather than surface similarity.

Selection criteria typically include:

Category alignment

Revenue structure similarity

Margin profile comparability

Stage calibration

Risk exposure

The objective is not to extract an average multiple.

It is to construct a defensible valuation range grounded in structural logic.

A single-point valuation invites negotiation. A range supported by articulated drivers invites calibration.

Translating Structure Into Investor Confidence

AI valuation discussions rarely break down because of ambition.

They break down because structural risk is not clearly articulated.

When category alignment, revenue durability, margin architecture, and capital efficiency are mapped correctly, valuation becomes less about negotiation and more about calibration.

The difference is subtle but material.

Instead of defending a headline multiple, the conversation shifts to explaining structural positioning.

That shift narrows dispersion.

It reduces assumption-driven friction.

It creates alignment around risk rather than argument around price.

For companies preparing for a funding round, evaluating a strategic transaction, or revisiting internal valuation benchmarks, the goal is not to inflate expectations.

It is to construct a defensible range that withstands scrutiny.

Valuation is not a single number.

It is a structured interpretation of risk, grounded in economic mechanics and market context.

Preparing for a Valuation Decision?

Share your stage and context. We’ll outline how the valuation should be framed, which assumptions matter most, and where investor scrutiny will concentrate.

A 15 to 20 minute strategy call to understand the valuation context and define the right scope.

- 1 AI startup valuation is not just about revenue multiples. Investors evaluate category positioning, revenue quality, scalability, margin structure, product defensibility, and the assumptions behind the financial model before accepting a valuation range.

- 2 AI companies are not valued as one market. Infrastructure, applied AI, workflow automation, vertical AI, agentic software, and AI-enabled services can attract very different valuation ranges because investors underwrite different risk profiles.

- 3 The strongest valuations connect technical differentiation to commercial execution. A model, product, or AI capability only supports valuation when it translates into adoption, retention, pricing power, or measurable customer value.

- 4 Investor-grade valuation work requires both comps and operating logic. Public AI comps, private funding rounds, and M&A transactions provide market context, but the valuation still depends on how the company grows, monetizes, and scales.

- 5 Financial models need to reflect AI-specific cost structures. Compute costs, model dependency, data requirements, implementation work, gross margin path, and support intensity can materially change how investors assess valuation.

- 6 A defensible AI valuation narrative is built around underwriting logic. The goal is not to present the highest possible multiple. It is to explain why the company deserves its position inside the valuation range.