Fintech Financial Modeling: How Investors Evaluate Revenue, Risk, and Valuation

Fintech models are not evaluated by structure alone. Investors focus on whether the revenue engine is durable, how margins evolve as volume scales, and whether growth improves capital efficiency instead of masking risk.

This guide explains how fintech financial models are reviewed during fundraising, board discussions, and M&A diligence. It focuses on the drivers investors test first: take rates, payment volume mechanics, margin layering, credit exposure, regulatory pressure, and scenario logic that holds up under scrutiny.

Below is a quick overview before we go deeper into the framework.

TL;DR

Topics covered in this article

- Why Fintech Models Are Evaluated Differently

- The Drivers Investors Pressure-Test First in Fintech Models

- Where Most Fintech Financial Models Break

- How Finro Structures Fintech Financial Models

- How Market Dynamics Shape Fintech Modeling Assumptions

- When Founders Typically Bring Finro Into a Fintech Modeling Project

- Summary

- Key Takeaways

- Answers to the Most Asked Questions

Why Fintech Models Are Evaluated Differently

Financial models in fintech are rarely assessed as simple growth forecasts. Investors look first at how revenue is generated, how risk accumulates inside the margin structure, and whether scale improves efficiency or simply expands exposure.

Two companies can report similar revenue growth yet receive very different feedback during diligence. The difference usually sits inside the mechanics of the model: how payment volume converts into revenue, how credit risk flows through the P&L, and whether margins improve as infrastructure scales.

Because fintech sits between software and financial services, investors expect models to explain not only growth but also the underlying economic engine. Assumptions that might be acceptable in a traditional SaaS forecast often raise immediate questions when applied to payments, lending, or embedded finance.

A strong fintech financial model shows how revenue compounds without introducing hidden fragility. It connects operational drivers to financial outcomes in a way that allows investors to understand both upside and downside without guessing.

Revenue quality matters more than growth speed

In fintech, growth alone rarely supports a strong narrative. Investors evaluate how durable that growth is and how it is produced. Take rates, transaction volume, and customer concentration often matter more than headline ARR expansion.

A model that scales through increased volume but ignores pricing pressure or regulatory cost signals usually breaks during diligence. Clear visibility into revenue sources, recurring behavior, and exposure to external partners helps investors understand whether growth reflects real adoption or temporary momentum.

This is why fintech financial models tend to start with drivers such as transaction flow, account activity, or credit utilization rather than top-down revenue targets. The structure of the model itself signals whether the company understands its own economics.

Margin structure signals risk before revenue does

Margin behavior often reveals risk earlier than revenue trends. Infrastructure-heavy businesses may carry strong gross margins but require significant operational investment to maintain compliance and uptime. Lending models may show strong top-line performance while hiding volatility inside loss assumptions or funding costs.

Investors read margin layering as a map of operational risk. They look at how costs move relative to volume, where external dependencies sit, and whether scale actually improves unit economics. When a model treats margin as a static percentage, it usually suggests that the underlying mechanics have not been fully tested.

Fintech models that clearly separate processing costs, partner fees, risk reserves, and compliance overhead tend to generate more constructive conversations. They allow investors to understand not only where profit might come from, but also what could slow it down.

How Investors Read Fintech Models vs How Founders Usually Build Them

| How founders often build fintech models | How investors actually read them |

|---|---|

| Start from a revenue target | Start from transaction mechanics, pricing, and margin flow |

| Assume take rate expansion without friction | Stress-test pricing power, competitive pressure, and compliance drag |

| Model gross margin as a flat percentage | Separate processing costs, partner fees, and infrastructure layers |

| Focus on top-line growth speed | Focus on capital efficiency and retention durability |

| One static forecast | Multiple scenarios tied to payment volume, risk exposure, and CAC |

| Model built mainly for fundraising decks | Model used to understand operational risk and valuation range |

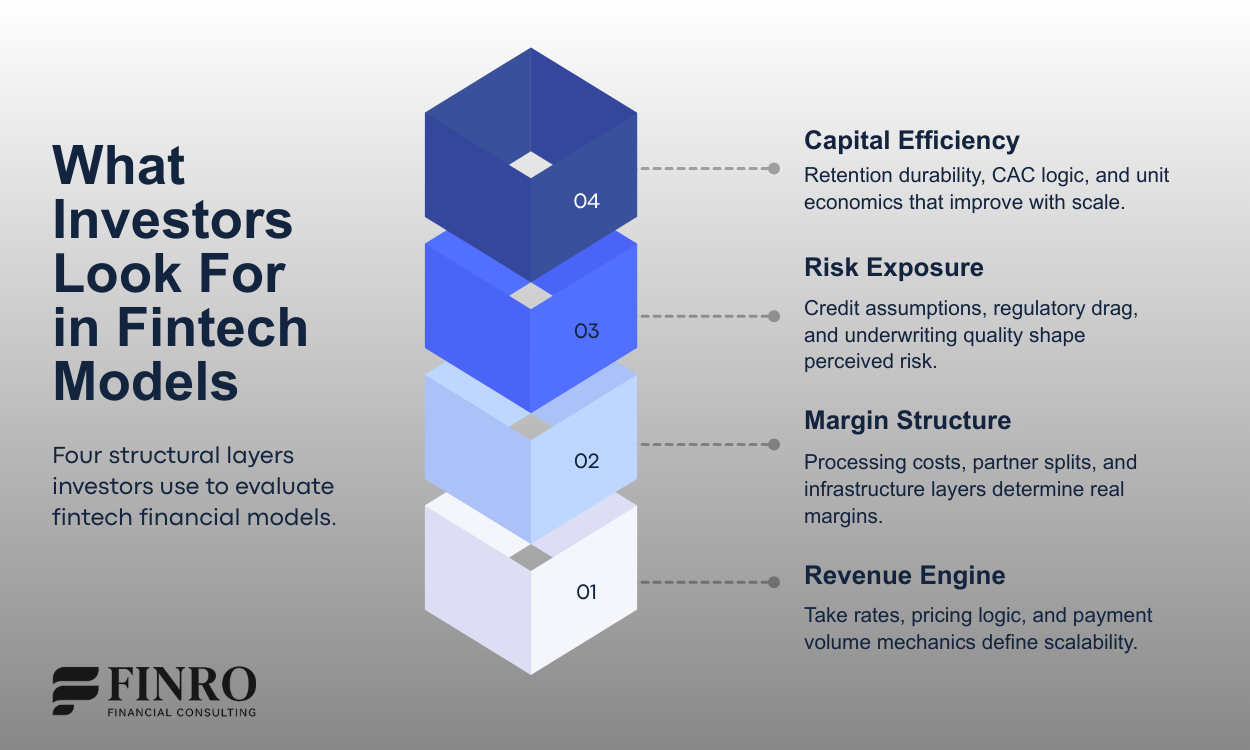

The Drivers Investors Pressure-Test First in Fintech Models

Fintech financial models are rarely evaluated through headline growth alone.

Investors tend to focus on a small set of structural drivers that reveal whether revenue can scale without increasing risk or capital intensity.

Most diligence conversations move quickly past formatting or spreadsheet structure. The real discussion starts once the model exposes how money actually flows through the system.

Below are the areas investors tend to examine first.

Take rates and payment volume mechanics

Many fintech models present revenue as a simple growth curve. Investors instead look for the mechanics behind it.

Payment volume, transaction frequency, customer mix, and pricing logic often matter more than top-line forecasts. A small change in take rate assumptions or payment behavior can materially shift margin outcomes and long-term valuation narratives.

Models that separate volume drivers from pricing drivers tend to hold up better under scrutiny because they allow investors to test scenarios without rebuilding the entire structure.

Margin layering across infrastructure and applications

Fintech margins rarely sit in a single line. They evolve through layers.

Infrastructure platforms often show stable but thinner gross margins that expand with scale. Application-level fintech products may present higher initial margins but carry heavier customer acquisition or servicing costs.

Strong models reflect this distinction clearly. Instead of presenting a single blended margin, they show where revenue originates and how cost structure shifts as the company grows.

This is where investors start assessing durability rather than just growth speed.

Credit exposure and regulatory drag

Credit products, lending models, and certain embedded finance structures introduce risk that standard SaaS assumptions do not capture.

Loss provisioning, capital requirements, compliance costs, and regulatory timelines can alter cash flow behavior long before revenue changes appear.

When these elements are missing or simplified, investors often discount projections because the model does not reflect real operating constraints.

Retention, cohorts, and capital efficiency

Retention in fintech is not only a product metric. It shapes how efficiently capital turns into revenue.

Cohort performance, payment volume expansion within existing accounts, and customer lifetime behavior influence how aggressively investors price growth. Models that connect retention assumptions to revenue expansion tend to feel more grounded than those relying solely on acquisition growth.

This is also where investors start linking financial modeling to valuation logic, even if the discussion is not explicitly framed around multiples.

Where Most Fintech Financial Models Break

Fintech financial models rarely fail because of formatting or spreadsheet complexity. Most break because the structure hides how money actually flows through the business. Investors are not looking for a polished template. They look for whether the model exposes risk, margin reality, and capital efficiency under pressure.

Across fundraising reviews, board discussions, and diligence work, the same structural issues appear repeatedly. Below are the patterns investors tend to identify first.

Revenue is modeled before transaction mechanics are defined

Many fintech models begin with a revenue target and work backward into volume assumptions. From an investor perspective, this reverses the logic. Revenue in fintech is an output of transaction mechanics, pricing structure, and partner economics.

When payment volume, lending exposure, or platform activity is not modeled at the driver level, it becomes impossible to understand how growth scales operationally. Investors want to see the path from transaction flow to monetization, not just a top-line projection that assumes pricing power holds constant.

Models that anchor revenue to real usage signals tend to hold up longer in diligence conversations because they show how growth behaves under different scenarios.

Risk exposure is hidden inside assumptions

Gross margin is often presented as a single percentage that improves over time. In fintech, this usually raises more questions than confidence.

Infrastructure fees, processing costs, partner revenue share, fraud exposure, and compliance overhead all influence margin structure differently. When these layers are collapsed into one assumption, the model stops reflecting operational reality.

Investors look for clarity on how margin evolves as volume grows. They want to understand which costs scale linearly, which compress over time, and which introduce structural risk. A layered margin view signals that the model reflects how fintech businesses actually operate.

Risk exposure hidden inside optimistic scenarios

Credit exposure, regulatory pressure, and reserve requirements often sit inside high-level assumptions rather than visible drivers. From a founder’s perspective this can keep the model clean. From an investor’s perspective it makes risk difficult to evaluate.

Risk is not just about downside scenarios. It influences the valuation range, capital requirements, and the durability of long-term margins. When risk drivers are transparent, conversations move faster because investors can understand how sensitive the business is to changing market conditions.

Models that expose risk clearly tend to produce more productive discussions than models that smooth volatility through averages.

Scenario logic is missing or disconnected from drivers

Many fintech models include a base case, an upside case, and a downside case. The issue is rarely the existence of scenarios. The issue is that they are not connected to real operating drivers.

If payment volume, pricing, or retention assumptions do not shift meaningfully between scenarios, investors struggle to understand what actually changes. Scenario modeling becomes most useful when it shows how different market conditions affect capital efficiency and margin behavior.

When scenarios are tied directly to transaction mechanics and cost structure, the model becomes a decision tool rather than a static forecast.

How Finro Structures Fintech Financial Models

Most fintech models fail because they start from spreadsheet structure instead of business mechanics. The goal is not to build a larger model. The goal is to make the financial logic reflect how revenue actually flows through infrastructure, risk layers, and capital requirements.

When we work on fintech financial modeling projects, the process usually starts by mapping operational drivers before touching formatting. Investors rarely debate whether a sheet looks clean. They focus on whether the model exposes the true economics of the business.

Driver-Based Revenue Architecture

Instead of starting from a top line growth assumption, fintech models need to be built from transaction logic. Payment volume, pricing structure, partner splits, and infrastructure costs must flow through the model in a way that mirrors real operations.

A driver-based architecture usually includes:

Volume mechanics tied to customer behavior

Pricing layers that reflect take rates and fee structures

Revenue streams separated by infrastructure and application logic

Margin flow that evolves as scale increases

This structure makes it easier to explain how growth translates into predictable revenue rather than headline expansion.

Scenario Logic Investors Actually Ask For

Investors rarely review a single forecast. They look for models that show how outcomes change when core drivers move.

Typical scenario questions include:

What happens to margins if payment costs increase?

How sensitive is growth to CAC efficiency or retention changes?

Does regulatory pressure reduce scalability?

How does credit exposure change capital requirements?

A strong fintech model connects scenarios to operational drivers rather than adjusting revenue percentages manually. This allows founders to show how risk and scalability interact inside the model.

Connecting Financial Models to Valuation Narratives

Even when the article focuses on modeling, investors still interpret every financial model as a signal about valuation. The structure of the model shapes how risk, scalability, and capital efficiency are perceived.

When revenue drivers, margin layers, and risk exposure are visible, the model becomes easier to defend in fundraising and diligence discussions. Instead of debating assumptions, the conversation moves toward strategy.

The goal is not to push a valuation outcome. The goal is to create a financial model that supports a coherent investor narrative built on measurable drivers.

Want a model that holds up in investor conversations?

Share your stage and goal, and we’ll tell you what structure fits and what we’d need to build a model that’s decision-ready.

Typical next step: a 15 to 20 minute strategy call.

How Market Dynamics Shape Fintech Modeling Assumptions

Fintech financial models do not fail because spreadsheets are wrong.

They fail because the assumptions behind them do not reflect how the market actually behaves.

Unlike traditional SaaS, fintech revenue depends on infrastructure partners, regulatory exposure, pricing pressure, and capital availability. Small changes in these areas can reshape margins or growth expectations quickly.

Investors understand this. When reviewing a fintech model, they rarely ask whether the formulas work. They ask whether the assumptions reflect real market dynamics.

Pricing pressure rarely shows up in early projections

Many fintech models assume stable or expanding take rates. In practice, pricing often compresses as volume grows or competition intensifies.

Payment processors, embedded finance platforms, and lending infrastructure providers frequently face margin pressure once scale attracts new entrants. Models that assume linear take rate expansion tend to overstate long-term revenue durability.

Investors typically stress-test:

how pricing behaves at scale

whether gross margin expansion depends on unrealistic assumptions

how partner economics evolve over time

Regulatory and compliance costs change margin structure

Fintech growth introduces operational complexity that many early models underestimate.

As transaction volume increases, compliance requirements, reserve logic, fraud prevention, and licensing costs often expand alongside revenue. These are not one-time expenses. They reshape cost structure.

Models that treat compliance as a fixed overhead tend to misrepresent future margins. Investors instead look for layered cost assumptions tied to volume, geography, or product expansion.

Capital availability influences growth more than projections suggest

Growth assumptions in fintech models often rely on continuous access to capital or favorable market conditions.

When funding environments tighten, lending products slow, marketing efficiency shifts, and customer acquisition dynamics change. A model that works during expansion cycles may break quickly during market resets.

This is why investors look for scenario logic that connects growth to capital efficiency rather than headline revenue targets.

Infrastructure versus application dynamics require different modeling logic

Infrastructure fintech platforms and application-layer fintech companies behave differently at scale.

Infrastructure businesses often show lower initial margins but stronger long-term operating leverage. Application-layer products may scale revenue faster but carry higher churn or acquisition costs.

Models that apply a single growth or margin framework across all fintech segments fail to capture these structural differences. Investors expect the model architecture to reflect where the company sits in the ecosystem.

When Founders Typically Bring Finro Into a Fintech Modeling Project

Fintech founders rarely come in asking for a “better spreadsheet.”

They usually reach out when investor conversations shift from growth narratives to structural questions about revenue quality, margins, and risk.

The timing tends to follow clear inflection points. Each stage introduces different modeling pressures, and the model often needs to evolve faster than the business itself.

Below are the moments where the gap between internal planning and investor expectations becomes visible.

Pre-seed to Seed: turning assumptions into a driver model

Early fintech models often start as simplified forecasts built around revenue targets or user growth. That approach works for early planning, but investors quickly look for the underlying mechanics behind take rates, transaction volume, or lending exposure.

At this stage, the goal is not complexity. The goal is clarity.

Founders typically bring Finro in when they need to:

Translate a narrative into a driver-based structure

Separate pricing logic from payment volume assumptions

Show how early unit economics evolve as scale increases

The result is a model that explains how revenue is generated, not just how fast it grows.

Seed to Series A: cleaning revenue mechanics and margin layers

As fintech companies move toward institutional funding, questions shift toward margin durability and infrastructure economics.

Investors begin asking:

Where processing costs sit inside gross margin

How partner splits affect scalability

Whether pricing expansion is realistic under regulatory pressure

Many internal models still treat margins as static percentages. That creates friction in diligence.

At this stage, founders usually need a cleaner structure that maps cost layers and shows how margins change across infrastructure, lending, or embedded finance models.

Series A to Growth: scenario logic, risk exposure, and board readiness

Later stage fintech companies face a different challenge. The model is no longer just a fundraising artifact. It becomes a decision tool used by boards and internal teams.

Scenario logic becomes central.

Investors expect to see:

Payment volume sensitivity

Credit exposure stress testing

Capital efficiency tied to retention and cohort behavior

This is often where existing models break down. They were built to explain a story, not to test assumptions under pressure.

Bringing structure to scenarios helps founders move discussions away from opinions and toward measurable trade-offs.

M&A and diligence: defensible structure, not spreadsheet polish

During acquisitions or strategic reviews, buyers rarely focus on formatting. They focus on whether the model reflects operational reality.

The strongest fintech models in diligence share a few characteristics:

Drivers connected to real business mechanics

Clear separation between revenue layers and risk exposure

Assumptions that can be traced back to market benchmarks

This is usually when founders realize that a model built for internal planning needs to be reframed as a defensible narrative.

Instead of rebuilding everything from scratch, the work often involves restructuring the logic so the model explains how value is created and how risk is managed.

| Model Type | Revenue engine | Margin structure | Risk exposure | Model focus |

|---|---|---|---|---|

| Fintech Infrastructure | Usage, seats, API pricing, platform fees | High GM if cost-to-serve scales cleanly | Lower credit risk, higher platform dependency | Retention, expansion, volume-driven scaling |

| Payments | Take rate x payment volume | Processing costs and partner fees drive GM | Fraud, chargebacks, underwriting constraints | Unit economics by channel, volume sensitivity |

| Lending | Interest income, fees, origination volume | Cost of capital + loss provisions dominate | Credit losses, reserves, regulatory pressure | Downside cases, stress tests, loss curves |

| Embedded Finance | Revenue share via partners, attach rates | Margins depend on partner economics | Partner concentration, compliance overhead | Ramp assumptions, partner-led growth scenarios |

| Vertical Fintech | Hybrid: SaaS + take rate + services | Mix of subscription GM and transaction GM | Customer concentration, workflow lock-in risk | Cohorts, ARPA expansion, cross-sell mechanics |

Summary

Fintech financial models are rarely judged on structure alone. Investors look for clarity around how revenue is generated, how margins evolve as volume scales, and how risk flows through the business. Growth without durable economics does not carry the same weight it once did, especially across payments, lending, infrastructure, and embedded finance models.

Across this guide, the focus was not on building bigger forecasts, but on building models that explain how a fintech company actually operates. Take rates, payment volume mechanics, margin layering, regulatory pressure, and capital efficiency are not supporting details. They are the core signals investors use to assess durability.

The difference between an average fintech model and a strong one is rarely complexity. It comes from aligning assumptions with how the market really behaves and structuring scenarios that reflect real operating constraints. When those elements are clear, the financial model becomes more than a projection. It becomes a tool that supports strategy, investor conversations, and long term decision making.

Key Takeaways

Revenue quality carries more weight than headline growth. Investors focus on payment volume mechanics, pricing logic, and whether take rates can hold under competitive and regulatory pressure.

Margin structure tells a deeper story than top line expansion. Processing costs, partner fees, and infrastructure dependencies shape gross margin evolution long before profitability appears.

Risk exposure is part of the model, not a footnote. Credit assumptions, compliance costs, and reserve requirements influence valuation narratives and scenario planning.

Capital efficiency is the signal investors track over time. Retention durability, cohort behavior, and unit economics determine whether growth translates into predictable performance.

Scenario logic matters more than forecast precision. Models built with clear drivers and realistic operating constraints hold up far better in diligence and board discussions.

Strong fintech models connect strategy to valuation outcomes. When assumptions reflect how the market actually works, the model becomes a framework for decision making rather than a static projection.

Ready to turn your fintech model into a decision tool?

If you are revisiting structure, preparing for fundraising, or pressure-testing assumptions, we can help you rebuild the model around drivers investors actually evaluate.

Typical next step: a short strategy call to understand your niche, stage, and modeling goals.

Answers to the Most Asked Questions

-

Fintech models are driven by transaction mechanics rather than subscription growth alone. Payment volume, take rates, processing costs, credit exposure, and regulatory friction all influence how revenue and margins evolve. A SaaS structure often misses these layers, which is why fintech models require more driver-based architecture.

-

Most investors scan for three signals: how revenue is generated, how margins behave as scale increases, and where operational risk sits inside the model. They rarely read every tab. Instead, they evaluate whether the core drivers connect logically and whether assumptions reflect real market constraints.

-

Not necessarily. Complexity does not create credibility. What matters is clarity around transaction flow, pricing logic, and capital requirements. A simple driver-based model that explains how the business works is usually more effective than a heavy forecast filled with unsupported assumptions.

-

They should reflect how the product is actually used. Investors expect to see realistic volume ramps, segmentation between customer types, and clear logic behind pricing. Flat take rate assumptions without operational context tend to raise more questions during diligence.

-

Yes. Even when risk exposure is indirect, investors want to understand how compliance costs, reserves, or underwriting assumptions affect margins over time. Ignoring these elements often leads to valuation discounts later in the process.

-

Usually when the model moves from internal planning to investor conversations. Fundraising, strategic partnerships, and M&A discussions often require restructuring assumptions so the narrative aligns with how investors interpret fintech risk and scalability.