Startup Financial Projections: What Investors Actually Look For

Startup financial projections sit at the center of nearly every fundraising discussion, yet they are often misunderstood. Many founders treat projections as a forecast of future revenue, focusing mainly on how the curve grows over time.

Investors usually see them differently.

A projection is not simply a prediction of where a company might end up. It is a framework that explains how the business behaves as it grows. The numbers themselves matter, but the real focus is on the mechanics underneath them: what drives revenue expansion, how margins evolve as the company scales, and how much capital is required to reach the next stage.

Those mechanics typically come from the structure of the underlying financial model. When founders build projections through disciplined startup financial modeling, the forecast becomes easier for investors to interpret because the assumptions behind growth, costs, and capital needs are clearly visible.

Because of this, projections that look convincing on the surface can still fail under investor scrutiny. Smooth growth curves, fixed cost assumptions, and optimistic timelines often hide the operating realities that determine whether a startup can execute its plan. Without an investor-ready financial model supporting the forecast, projections may appear impressive but provide little insight into how the business actually scales.

When investors review startup financial projections, they are typically trying to answer a different set of questions. What actually drives revenue growth? How do unit economics evolve as the company scales? Which costs increase with usage, and which create operating leverage? How sensitive is the plan to changes in hiring, pricing, or conversion rates?

This article explains how startup financial projections are evaluated in practice, why many forecasts fail investor scrutiny, and what separates projections that simply look good from projections that actually help investors understand how a business works.

TL;DR

Topics covered in this article

What Startup Financial Projections Are Actually Supposed to Do

Startup financial projections are often treated as predictions about future performance. In practice, their role is very different. Investors rarely expect projections to forecast revenue with precision, especially at the early stages of a company.

Instead, projections help explain how the business behaves as it grows. They translate the operating mechanics of the company into financial outcomes so that investors can understand the relationship between growth, cost structure, and capital requirements.

When projections are built on clear drivers, they allow investors to see how revenue expands, how margins evolve, and how the company plans to deploy capital over time. In that sense, projections function less as a forecast and more as a structured representation of the business.

This is also why projections are closely connected to the structure of the underlying financial model. Investors typically analyze projections through the same lens they use to evaluate the broader financial framework of the company.

When that structure is visible, projections become easier for investors to evaluate. Instead of debating the exact shape of the forecast curve, they can focus on the assumptions that generate it and assess whether those assumptions reflect the operational reality of the business.

How investors interpret startup financial projections

Founders often focus on the shape of the forecast curve. Investors focus on the mechanics that produce that curve.

| Forecast mindset | Investor mindset |

|---|---|

| Revenue growth curve | Revenue drivers (acquisition, pricing, retention) |

| Static margins | Unit economics behavior over time |

| Flat cost assumptions | Operational scaling mechanics |

| Single scenario forecast | Sensitivity to key assumptions |

| Long-term revenue targets | Capital requirements and runway |

Why Startup Projections Fail Investor Scrutiny

Most startup projections do not fail because the spreadsheet is wrong.

They fail because the model underneath the projection is not doing the job investors expect it to do.

A projection is only as credible as the operating logic behind it. When the logic is thin, investors stop debating the numbers and start debating whether the team understands the business.

Here are the patterns that show up most often.

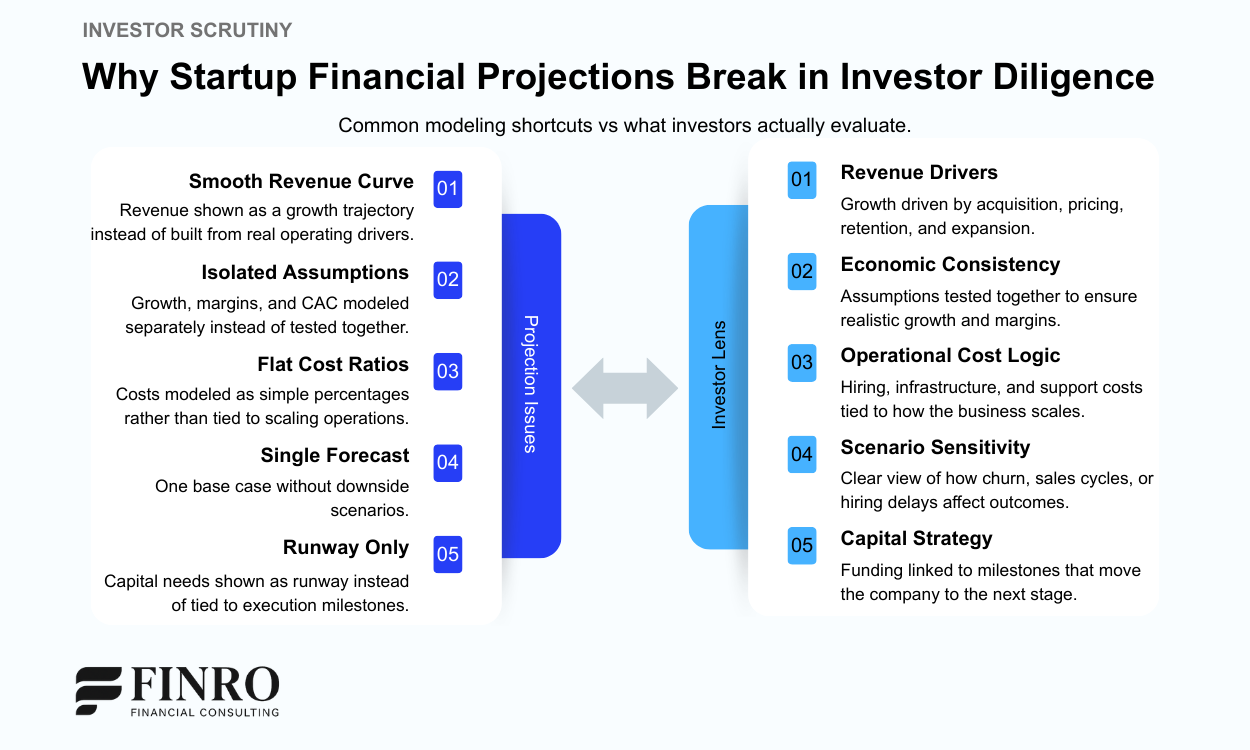

1) Growth is modeled as a curve, not a mechanism

Revenue is frequently forecast as a smooth trajectory toward a target. Investors will immediately ask what produces that curve: acquisition capacity, conversion behavior, expansion, retention, pricing, and timing. If those mechanics are not explicit, the projection reads like a narrative, not an operating plan.

2) Assumptions are “clean” in isolation but incompatible together

Founders often model strong growth, improving margins, and stable CAC at the same time. Each assumption might be plausible alone. Together, they can be economically inconsistent. Investor scrutiny often focuses on the interaction between assumptions, not the assumptions themselves.

3) Costs are treated as static, while operations are dynamic

Many models use flat percentages or linear cost growth. Real businesses scale unevenly: headcount steps up in waves, infrastructure scales with usage, onboarding and support intensity shifts by segment, and sales capacity takes time to ramp. If the model does not reflect that, the projection looks overconfident.

4) The model cannot explain downside scenarios

Investors rarely accept a single “base case.” They test what happens if sales cycles extend, conversion drops, churn increases, hiring slips, or costs rise. A credible model makes it easy to see how downside flows into margins, runway, and capital needs. When the model cannot do that quickly, confidence drops.

5) Funding plans are disconnected from milestones

A projection should make the fundraising logic obvious: what this round funds, what milestones it buys, and when the next stage becomes financeable. When the capital plan is presented as runway only, investors assume the plan is not anchored to execution reality.

6) Inputs are adjustable, but the model is not decision-ready

A model can be editable and still not usable. Investors are looking for a structure that answers specific questions fast: what moves the outcome, what breaks first, and what has to be true for the story to hold. If the model doesn’t support that workflow, the projection feels fragile.

The common thread is simple: investors are not buying the forecast. They are underwriting the mechanics.

When those mechanics are visible and internally consistent, the projection becomes a credible valuation input. When they are not, the projection becomes something investors discount heavily, even if the numbers look attractive.

What a Credible Startup Financial Model Actually Shows

Once the projection shortcuts are removed, the role of the financial model becomes much clearer. A strong model does not try to predict the exact outcome of the business. Instead, it explains how the company behaves as it grows and how changes in the underlying drivers affect the financial trajectory.

For investors, the value of the model lies in its ability to make the mechanics of the business visible. When those mechanics are clear, projections become easier to interpret and the discussion shifts from debating the numbers to evaluating the operating assumptions behind them.

Several elements usually determine whether a financial model provides that clarity.

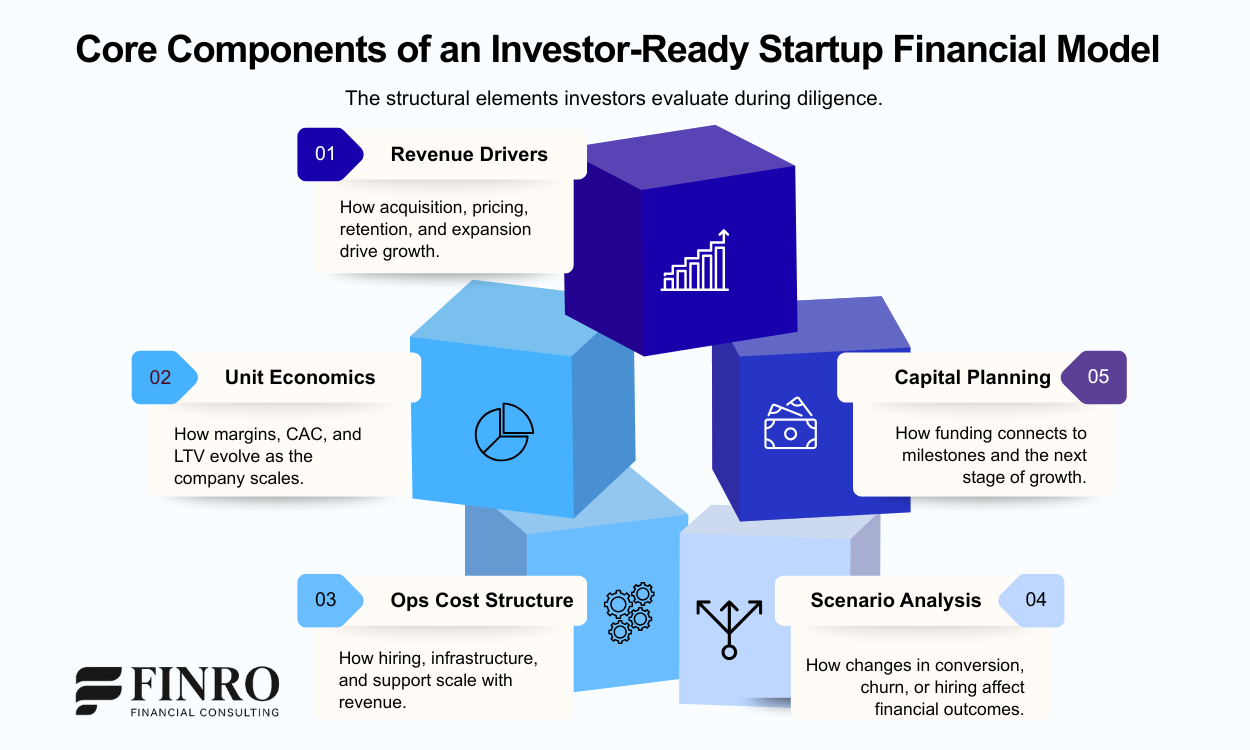

Revenue drivers and operating mechanics

Revenue should be built from the mechanisms that actually generate growth. That typically includes acquisition capacity, conversion rates, pricing structure, retention, and expansion. When these drivers are explicit, investors can see how growth is produced rather than simply observing the outcome.

Unit economics and margin behavior

A credible model shows how margins evolve as the company scales. This includes how gross margin behaves with usage, how sales efficiency changes with scale, and how customer acquisition interacts with lifetime value. Investors use these relationships to evaluate whether growth improves the economics of the business or puts pressure on them.

Operational cost structure

Costs rarely grow in a straight line. Hiring plans, infrastructure, customer support, and product development typically expand in stages as the company grows. A structured model reflects these operational realities so investors can understand how the organization scales alongside revenue.

Scenario sensitivity

Investors rarely evaluate a single base case. They want to understand how the business behaves under different conditions such as slower acquisition, longer sales cycles, higher churn, or delayed hiring. A model that makes these sensitivities visible helps investors understand both the resilience and the risk of the plan.

Capital planning and milestones

Finally, the model should make the capital strategy clear. Hiring plans, infrastructure investments, and operational expansion should connect directly to funding milestones. When that connection is visible, investors can see how each round of capital supports the company’s next stage of growth.

When these elements are present, the financial model becomes more than a projection tool. It becomes a framework that allows investors to evaluate how the business operates, how risk behaves, and how capital converts into growth.

How Financial Models Shape Investor Conversations

Once the structure of the financial model is clear, projections start serving a much more practical purpose during fundraising. They become a tool for structuring the conversation between founders and investors rather than simply presenting a forecast.

In most investor meetings, the discussion rarely centers on the exact numbers in the model. Instead, investors focus on the assumptions that generate those numbers and how sensitive the outcome is to changes in those assumptions.

A well-structured financial model makes these discussions significantly easier because the drivers behind the projections are visible.

When revenue is broken into acquisition capacity, conversion behavior, pricing, and retention, investors can evaluate how realistic the growth path is. When the cost structure reflects how the organization actually scales, investors can assess whether margins improve as the company grows or whether operational complexity will absorb those gains.

The model also becomes an important reference point for evaluating risk. Investors often test how the business performs under different conditions: slower customer acquisition, longer sales cycles, higher churn, or delayed hiring. When the model makes those scenarios easy to explore, it gives investors a clearer view of both downside exposure and upside potential.

Capital planning is another area where the financial model directly shapes investor conversations. Rather than simply presenting runway, the model can show how funding connects to specific milestones such as product development, market expansion, or sales capacity. This allows investors to understand what the next round of capital is expected to achieve.

When the model provides this level of clarity, the conversation shifts away from defending projections and toward evaluating the strategic path of the business. Investors are no longer trying to interpret the numbers. They are assessing whether the underlying mechanics of the company support the growth story being presented.

“If you need startup financial modeling expertise, Lior and Finro are as strong as it gets. They are fast, precise, and intuitively understand what a startup at your stage needs from a model. I’d hire Lior for FP&A any day, and I’d recommend Finro to anyone looking for serious financial support.”

Need a financial model that holds up under investor scrutiny?

Finro builds investor-ready startup financial models that make the revenue drivers, cost structure, and capital plan explicit, so the story holds when the questions get harder.Key Takeaways

Startup financial projections are not about predicting the future. Their primary role is to explain how the business behaves as it grows and how operating decisions translate into financial outcomes.

Investors evaluate the mechanics behind the numbers. Revenue drivers, cost structure, and capital planning matter far more than the shape of a growth curve.

Most projections fail because the operating logic is missing. Smooth growth curves, flat cost assumptions, and single-scenario forecasts rarely survive investor scrutiny.

A credible financial model makes the drivers of the business visible. When acquisition, retention, pricing, and operational scaling are explicit, projections become easier for investors to evaluate.

Scenario analysis and capital planning are central to investor discussions. Investors want to understand how the business behaves under different conditions and how funding connects to milestones.

When the structure is clear, projections become a decision framework. Instead of defending numbers, founders can focus on discussing strategy, execution, and the path to the next stage of growth.

Answers to the Most Asked Questions

-

Startup financial projections estimate how revenue, costs, and capital needs evolve as a company grows. Investors use them to understand how the business operates and how different assumptions affect financial outcomes.

-

Investors rarely focus on the forecast itself. Instead, they evaluate the drivers behind it, including acquisition capacity, pricing, retention, cost structure, and how capital supports the company’s growth milestones.

-

Projections often fail because they rely on simplified assumptions. Smooth growth curves, flat cost ratios, and single-scenario forecasts usually hide the operational mechanics investors want to evaluate.

-

A credible model typically includes revenue drivers, unit economics, operational cost structure, scenario analysis, and capital planning. These elements help investors understand how the business scales and how funding supports growth.

-

Most startups build their first structured financial model before raising institutional capital. A clear model helps founders test assumptions, plan hiring and spending, and communicate their strategy to investors.